Learning Modules Hide

Hide

- Chapter 1: Introduction to Derivatives

- Chapter 2: Futures and Forwards: Know the basics – Part 1

- Chapter 3: Futures and Forwards: Know the basics – Part 2

- Chapter 4: Introduction to Futures

- Chapter 5: Futures Terminology

- Chapter 6: Futures Trading – Part 1

- Chapter 7: Futures Trading – Part 2

- Chapter 8: Advanced Concepts in Futures

- Chapter 9: Participants in the Futures Market

- Chapter 1: Introduction to Derivatives

- Chapter 2: Introduction to Options

- Chapter 3: Options Terminology

- Chapter 4: Options Trading - Long Call (Call Buyer)

- Chapter 5: Options Trading - Short Call (Call Seller)

- Chapter 6: Options Trading - Long Put (Put Buyer)

- Chapter 7: Options Trading - Short Put (Put Seller)

- Chapter 8: Options Summary

- Chapter 9: Advanced Concepts in Options – Part 1

- Chapter 10: Advanced Concepts in Options – Part 2

- Chapter 11: Option Greeks – Part 1

- Chapter 12: Option Greeks – Part 2

- Chapter 13: Option Greeks – Part 3

- Chapter 1: Orientation on Option Strategies

- Chapter 2: Bull Call Spread

- Chapter 3: Bull Put Spread

- Chapter 4: Covered Call

- Chapter 5: Bear Call Spread

- Chapter 6: Bear Put Spread

- Chapter 7: Covered Put

- Chapter 8: Long Call Butterfly

- Chapter 9: Short Straddle

- Chapter 10: Short Strangle

- Chapter 11: Iron Condor

- Chapter 12: Long Straddle

- Chapter 13: Long Strangle

- Chapter 14: Short Call Butterfly

- Chapter 15: Protective Put

- Chapter 16: Protective Call

- Chapter 17: Delta Hedging

Chapter 16: Protective Call

When Abhinav’s boss asks him to suggest a strategy to hedge the short position of a stock, he recommends the Protective Call Option. In this chapter, we will view the details of this strategy.

Protective Call

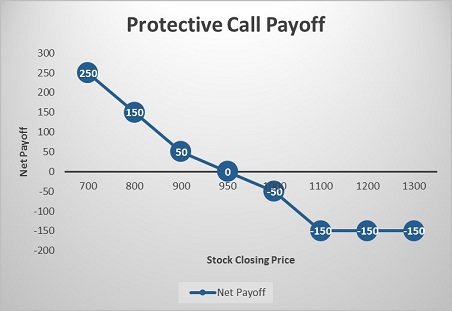

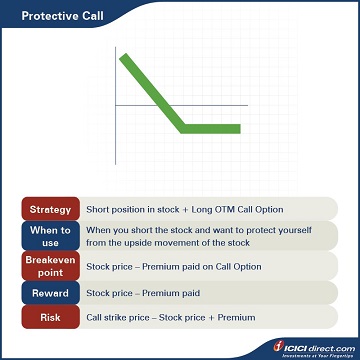

A Protective Call strategy is used to hedge the short position of a stock by purchasing an ATM or slightly OTM Call Option. This strategy works well in a scenario when you short the stock and want to protect yourself from the upside movement of the stock.

This position is also called Synthetic Long Put, but net payout is positive. You receive money on shorting the stock and pay the premium to buy a Call.

Strategy: Short position in stock + Long OTM Call Option

When to use: When you short the stock and want to protect yourself from the upside movement of the stock.

Breakeven: Stock price – Premium paid on Call Option

Maximum profit: Stock price – Premium paid

Maximum risk: Call strike price – Stock price + Premium

Let’s understand this with an example:

Assume that the spot price of ABC Ltd. is Rs. 1,000. Abhinav buys an ABC Ltd. OTM Call Option at a strike price of Rs. 1,100 at Rs. 50. He pays a total premium of Rs. 50. The breakeven point in this case will be Rs. 1,000 – Rs. 50 = Rs. 950.

Maximum profit will be limited to stock price – premium i.e. Rs. 1,000 – Rs. 50 = Rs. 950 when stock price becomes zero. The maximum risk in this position will be Rs. 1,100 – Rs. 1,000 + Rs. 50 = Rs. 150.

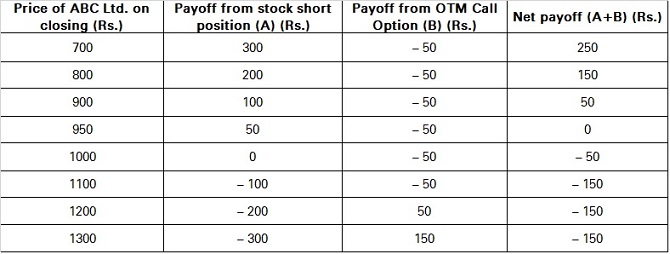

Let’s look at the cash flow in various scenarios:

Let us understand the payoff in various scenarios. It will give you a fair idea of how we have arrived at the above values.

If the stock closes at Rs. 800 on expiry: The long Call Option will expire OTM

The selling price of the stock = Rs. 1000

The purchase price of the stock on expiry = Rs. 800

So, the payoff from the spot position = Selling price – Purchase price = 1000 – 800 = Rs. 200

Premium paid on the OTM Call Option of strike price Rs.1100 = Rs. 50

Premium received on the OTM Call Option of strike price Rs. 1100 at expiry = Max {0, (Spot price – Strike price)} = Max {0, (800 – 1100)} = Max (0, – 300) = 0

So, the payoff from the OTM Call Option = Premium received – Premium paid = 0 – 50 = – Rs. 50

Net payoff = Payoff from the spot position + Payoff from OTM Call Option = 200 + (– 50) = Rs. 150

If the stock closes at Rs. 950 on expiry: The long Call Option will expire OTM

The selling price of the stock = Rs. 1000

The purchase price of the stock on expiry = Rs. 950

So, the payoff from the spot position = Selling price – Purchase price = 1000 – 950 = Rs. 50

Premium paid on the OTM Call Option of strike price Rs.1100 = Rs. 50

Premium received on OTM Call Option of strike price Rs. 1100 at expiry = Max {0, (Spot price – Strike price)} = Max {0, (950 – 1100)} = Max (0, – 150) = 0

So, the payoff from the OTM Call Option = Premium received – Premium paid = 0 – 50 = – Rs. 50

Net payoff = Payoff from the spot position + Payoff from OTM Call Option = 50 + (– 50) = 0

If the stock closes at Rs. 1200 on expiry: The long Call Option will expire ITM

The selling price of the stock = Rs. 1000

The purchase price of the stock on expiry = Rs. 1200

So, the payoff from the spot position = Selling price – Purchase price = 1000 – 1200 = – Rs. 200

Premium paid on the OTM Call Option of strike price Rs.1100 = Rs. 50

Premium received on OTM Call Option of strike price Rs. 1100 at expiry = Max {0, (Spot price – Strike price)} = Max {0, (1200 – 1100)} = Max (0, 100) = Rs. 100

So, the payoff from the OTM Call Option = Premium received – Premium paid = 100 – 50 = Rs. 50

Net payoff = Payoff from the spot position + Payoff from OTM Call Option = (– 200) + 50 = – Rs. 150

Additional Read: Chapter 2: Introduction to Options

Summary

- A Protective Call strategy is used to hedge the short position of a stock by purchasing an ATM or slightly OTM Call Option.

- This strategy works well in a scenario when you short the stock and want to protect yourself from its upside movement.

- Breakeven: Stock price – Premium paid on Call Option

- Maximum profit: Stock price – Premium paid

- Maximum risk: Call strike price – Stock price + Premium

In the next chapter, we will look into Delta Hedging. This strategy allows you to hedge the risk associated with the change in delta due to the underlying asset's price movement.

Please Enter Email

COMMENT (0)