A Non Convertible debenture is a financial instrument that allows a private or public corporation to borrow money from investors. In other words, when an investor buys a corporate bond, he/she lends money to the company (Issuer). In exchange, the company promises to repay the money (Principal) on a specified date in future (Maturity). Until that date, the company makes regular payment to investors at a specified rate of interest (Coupon). Thus, through a corporate bond, a company gets the money it needs for business operations and investors get a pre-defined interest payment for a specified period in lieu of the money lent to the Issuer

Coupon – Interest paid to the investor periodically. Can range from monthly, quarterly, half-yearly to yearly.

Face Value – Value per bond paid out by Issuer on maturity or on exercise of call option by Issuer

Maturity date – The date on which Issuer repays principal amount.

Credit Rating – Quantified assessment of the creditworthiness of a borrower in general terms or with respect to a particular bond by Credit Rating Agencies

Call option on bonds – Gives issuer of the bond the option to call back the bond before its maturity and repay principal amount. Feature is common in perpetual bonds. The option is exercised by the issuer when interest rates decline and capital requirement can be met at lower cost.

YTM (Yield to Maturity) – Annualized return on the bond realized by an investor if bond is held to maturity.

Accrued Interest – Amount of interest earned on a debt but not yet collected. Interest starts accumulating from the last coupon payment date.

Clean Price – Price of the bond without accrued interest on that bond.

Dirty Price – Clean price of the bond + accrued interest = Dirty Price of the bond. It is the actual consideration paid by buyer of the bond to the seller. Is also known as settlement price of the bond.

Credit or Default Risk – Issuers inability to pay interest and/or principal payment due to weakening of creditworthiness. Can be partially mitigated by investing in high rated bonds

Duration Risk – Sensitivity of bond prices to change in interest rates. Higher coupon & higher number of years to maturity results in more price volatility to change in interest rate

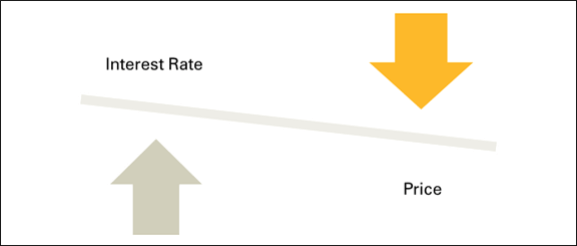

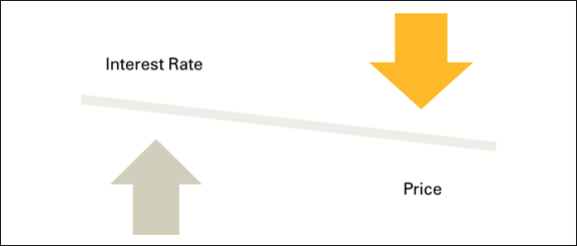

Interest Rate Risk – Change in price of bond to change in interest rates. Bond prices move opposite to the direction of interest rates. When interest rates fall, bond prices go up and vice versa.

Liquidity Risk – Lack of active trading on the bond may result in illiquidity. Bond holders are unable to find buyers for the bond and/or receive sub-optimal price on Sale.

Inflation Risk – Inflation rising above coupon rate resulting in negative real return. For example, if coupon is 6% and inflation rises to 7%, investors fall behind inflation by 1%

Call & Reinvestment Risk – Issuer redeeming principal prior to maturity and inability of buyer to find similar coupon through fresh investment. Witnessed in a falling interest rate scenario.

1. Bond yield is the return an investor realizes on a bond. It is the anticipated return on an investment, expressed as an annual percentage. For example, a 8% yield means that the investment averages 8% return each year till maturity. Yield is an important concept in bond investing. It is used to measure return of one bond against another and it enables investors to make informed decision while investing in bonds.

2. Yield is commonly measured in two ways, current yield and yield to maturity.

3. A) Current yield

4. The current yield is the annual return on the investment value of bond, regardless of its maturity. If you buy a bond at par, the current yield equals its coupon rate. Thus, the current yield on a par-value bond paying 8% is 8%. However, if the market price of the bond is higher or lower than par, the current yield will be different. For example, if you buy a Rs. 1000 bond with a 8% stated interest rate at Rs. 1100, your current yield would be 7.27% (Rs. 1000 x 0.08/Rs.1100).

5. B) Yield to maturity

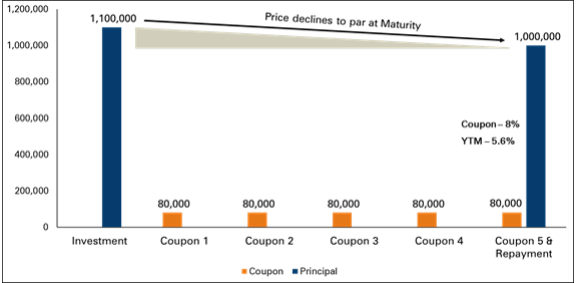

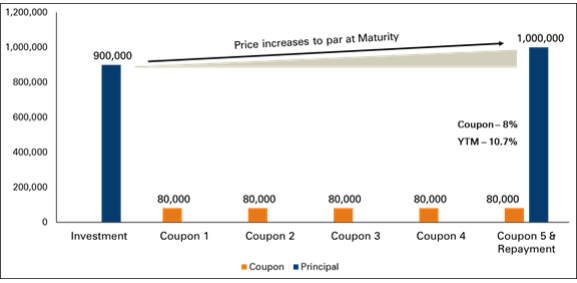

6. It is the total return an investor receives on a bond if held until maturity. It enables one to compare bonds with different maturities and coupon rates. Yield to maturity includes the current yield and the capital gain or loss you can expect if you hold the bond to maturity. If you pay Rs. 900 for a 5% coupon bond with a face value of Rs. 1,000 maturing five years from the date of purchase, you will earn not only Rs. 50 a year in interest but also another Rs. 100 when the bond’s issuer pays off the principal. By the same logic, if you buy that bond for Rs. 1,100, representing a Rs.100 premium, you will lose Rs. 100 at maturity

7. Example 1 - YTM illustration of a 5 year bond with 8% annual interest bought at Premium and held till maturity

8. Example 2 - YTM illustration of a 5 year bond with 8% annual interest bought at discount and held till maturity

Yield and prices are inversely propotional to each other

If the yield increases the prices are reduced and if yields reduces then prices moves up

Actual prices are also affected by the length of time left before the bond matures and by the likelihood that the issue will be called. But the underlying principle is the same, and it is the single most important thing to remember about the relationship between the market value of the bonds you hold and changes in current interest rates: As interest rates rise, bond prices fall; as interest rates fall, bond prices rise. The farther away the bond’s maturity or call date, the more volatile its price tends to be. Because of this relationship, the actual yield to an investor depends in large part on where interest rates stand on the day the bond is purchased

A credit rating is an opinion of a particular credit agency regarding the ability and willingness an entity (government, business, or individual) to fulfill its financial obligations in completeness and within the established due dates. A credit rating also signifies the likelihood a debtor will default. It is also representative of the credit risk carried by a bond. A credit rating is, however, not an assurance or guarantee of a kind of financial performance by a certain instrument of debt or a specific debtor.

| Symbols | |

|---|---|

| AAA (Highest Safety) | Instruments with this rating are considered to have the highest degree of safety regarding timely servicing of financial obligations. Such instruments carry lowest credit risk. |

| AA (High Safety) | Instruments with this rating are considered to have high degree of safety regarding timely servicing of financial obligations. Such instruments carry very low credit risk. |

| A (Adequate Safety) | Instruments with this rating are considered to have adequate degree of safety regarding timely servicing of financial obligations. Such instruments carry low credit risk. |

| BBB (Inadequate Safety) | Instruments with this rating are considered to have moderate degree of safety regarding timely servicing of financial obligations. Such instruments carry moderate credit risk. |

| BB (Moderate Risk) | Instruments with this rating are considered to have moderate risk of default regarding timely servicing of financial obligations. |

| B (High Risk) | Instruments with this rating are considered to have high risk of default regarding timely servicing of financial obligations. |

| C (Very High Risk) | Instruments with this rating are considered to have very high risk of default regarding timely servicing of financial obligations. |

| D (Default) | Instruments with this rating are in default or are expected to be in default soon. |

Top Mutual Funds

Top Mutual Funds