Learning Modules Hide

Hide

- Chapter 1: Introduction to Derivatives

- Chapter 2: Futures and Forwards: Know the basics – Part 1

- Chapter 3: Futures and Forwards: Know the basics – Part 2

- Chapter 4: Introduction to Futures

- Chapter 5: Futures Terminology

- Chapter 6: Futures Trading – Part 1

- Chapter 7: Futures Trading – Part 2

- Chapter 8: Advanced Concepts in Futures

- Chapter 9: Participants in the Futures Market

- Chapter 1: Introduction to Derivatives

- Chapter 2: Introduction to Options

- Chapter 3: Options Terminology

- Chapter 4: Options Trading - Long Call (Call Buyer)

- Chapter 5: Options Trading - Short Call (Call Seller)

- Chapter 6: Options Trading - Long Put (Put Buyer)

- Chapter 7: Options Trading - Short Put (Put Seller)

- Chapter 8: Options Summary

- Chapter 9: Advanced Concepts in Options – Part 1

- Chapter 10: Advanced Concepts in Options – Part 2

- Chapter 11: Option Greeks – Part 1

- Chapter 12: Option Greeks – Part 2

- Chapter 13: Option Greeks – Part 3

- Chapter 1: Orientation on Option Strategies

- Chapter 2: Bull Call Spread

- Chapter 3: Bull Put Spread

- Chapter 4: Covered Call

- Chapter 5: Bear Call Spread

- Chapter 6: Bear Put Spread

- Chapter 7: Covered Put

- Chapter 8: Long Call Butterfly

- Chapter 9: Short Straddle

- Chapter 10: Short Strangle

- Chapter 11: Iron Condor

- Chapter 12: Long Straddle

- Chapter 13: Long Strangle

- Chapter 14: Short Call Butterfly

- Chapter 15: Protective Put

- Chapter 16: Protective Call

- Chapter 17: Delta Hedging

Chapter 12: Long Straddle

There are different multi-leg Options strategies for various market views. If you are bullish about the market, then you can go in for a Bull Call Spread, Bull Put Spread or a Covered Call. If you are bearish, you can go for a Bear Call Spread, a Bear Put Spread or a Covered Put. Neutral view Options include the Long Call Butterfly, Short Straddle, Short Strangle or Iron Condor.

But what if your views don’t fall into any of these brackets? Are there Options strategies for scenarios such as when you have expectations of great volatility in the underlying asset but are unsure of your view of the market? Here, we will explore one such multi-leg Options strategy: A Long Straddle.

Long Straddle

A Straddle is a strategy that aims at capturing volatility in prices of the underlying asset. In a Long Straddle, the trader buys a Call together with a Put on the same underlying for the same expiry and strike price. The Options bought are normally ATM Options.

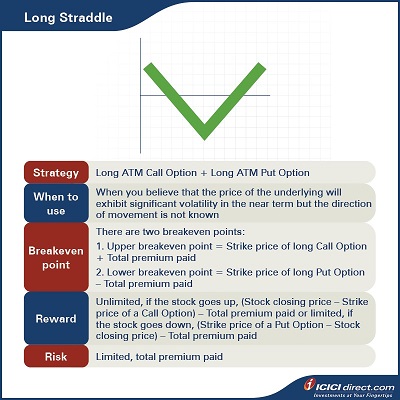

- This strategy is used when the trader believes that the price of the underlying will exhibit significant volatility in the near term, but the direction of movement is not known.

- The risk in Long Straddle is limited to the extent of premiums paid on the Options, but returns are unlimited.

Strategy: Long ATM Call Option (Leg 1) + Long ATM Put Option (Leg 2)

When to use: When you believe that the price of the underlying will exhibit significant volatility in the near term but the direction of movement is not known

Breakeven: There are two breakeven points:

1. Upper breakeven point = Strike price of long Call Option + Total premium paid

2. Lower breakeven point = Strike price of long Put Option – Total premium paid

Maximum profit: Unlimited, if the stock goes up, (Stock closing price – Strike price of a Call Option) – Total premium paid or limited, if the stock goes down, (Strike price of a Put Option – Stock closing price) – Total premium paid

Maximum risk: Limited, total premium paid

|

Did you know? Newsworthy events like unexpected earnings release from a company is the perfect fodder for a Long Straddle strategy. Since there is no way of knowing in advance what the results might be, a Long Straddle can help you profit from a big move. |

Let’s understand this strategy with an example:

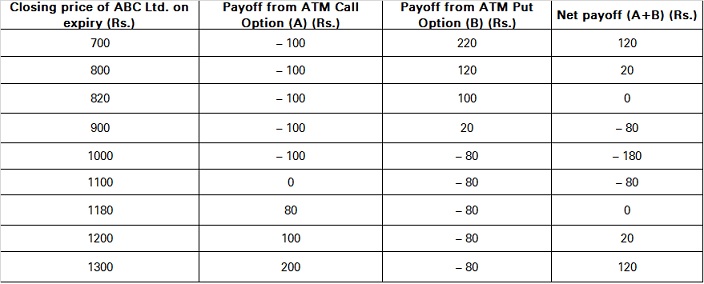

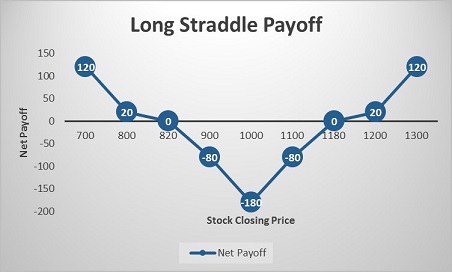

Let us assume that you buy ABC Ltd. ATM Call and Put Options of strike price Rs. 1,000 at Rs. 100 and Rs. 80 respectively. You paid a total premium of Rs. 100 + Rs. 80 = Rs. 180. This will be the maximum loss. You will earn a profit if the stock moves more than 180 points in any direction i.e. either above Rs. 1,180 or below Rs. 820.

Let’s look at the cash flow in various scenarios:

Let us understand the payoff in various scenarios. This will give you a fair idea of how we have arrived at the above values.

If the Stock closes at Rs. 700 on expiry: Leg 1 expires OTM while leg 2 expires ITM

Leg 1: Premium paid on the ATM Call Option of strike price Rs. 1000 = Rs. 100

Premium received on ATM Call Option of strike price Rs. 1000 at expiry = Max {0, (Spot price – Strike price)} = Max {0, (700 – 1000)} = Max (0, – 300) = 0

So, the payoff from the ATM Call Option = Premium received – Premium paid = 0 – 100 = – Rs. 100

Leg 2: Premium paid on the ATM Put Option of strike price Rs. 1000 = Rs. 80

Premium received on ATM Put Option of strike price Rs. 1000 at expiry = Max {0, (Strike price – Spot price)} = Max {0, (1000 – 700)} = Max (0, 300) = Rs. 300

So, the Payoff from the OTM Put Option = Premium received – Premium paid = 300 – 80 = Rs. 220

Net Payoff = Payoff from OTM Call Option + Payoff from OTM Put Option = (– 100) + 220 = Rs. 120

If the Stock closes at Rs. 1000 on expiry: Both the legs expire ATM

Leg 1: Premium paid on the ATM Call Option of strike price Rs. 1000 = Rs. 100

Premium received on ATM Call Option of strike price Rs. 1000 at expiry = Max {0, (Spot price – Strike price)} = Max {0, (1000 – 1000)} = Max (0, 0) = 0

So, payoff from the ATM Call Option = Premium received – Premium paid = 0 – 100 = – Rs. 100

Leg 2: Premium paid on the ATM Put Option of strike price Rs. 1000 = Rs. 80

Premium received on ATM Put Option of strike price Rs. 1000 at expiry = Max {0, (Strike price – Spot price)} = Max {0, (1000 – 1000)} = Max (0, 0) = 0

So, the Payoff from the OTM Put Option = Premium received – Premium paid = 0 – 80 = – Rs. 80

Net Payoff = Payoff from OTM Call Option + Payoff from OTM Put Option = (– 100) + (– 80) = – Rs. 180

If the Stock closes at Rs. 1300 on expiry: Leg 1 expires ITM while leg 2 expires OTM

Leg 1: Premium paid on the ATM Call Option of strike price Rs. 1000 = Rs. 100

Premium received on ATM Call Option of strike price Rs. 1000 at expiry = Max {0, (Spot price – Strike price)} = Max {0, (1300 – 1000)} = Max (0, 300) = Rs. 300

So, the payoff from the ATM Call Option = Premium received – Premium paid = 300 – 100 = Rs. 200

Leg 2: Premium paid on the ATM Put Option of strike price Rs. 1000 = Rs. 80

Premium received on ATM Put Option of strike price Rs. 1000 at expiry = Max {0, (Strike price – Spot price)} = Max {0, (1000 – 1300)} = Max (0, – 300) = 0

So, the Payoff from the OTM Put Option = Premium received – Premium paid = 0 – 80 = – Rs. 80

Net Payoff = Payoff from OTM Call Option + Payoff from OTM Put Option = 200 + (– 80) = Rs. 120

Additional Read: Chapter 6: Options Trading – Long Put (Put Buyer)

Summary

- A Straddle is a strategy which aims at capturing volatility in prices of the underlying asset.

- In a Long Straddle, the trader buys a Call together with a Put on the same underlying for the same expiry and strike price. The Options bought are normally ATM Options.

- Breakeven: There are two breakeven points:

- Upper breakeven point = Strike price of long Call Option + Total premium paid

- Lower breakeven point = Strike price of long Put Option – Total premium paid

- Maximum profit: Unlimited, (Stock closing price – Strike price of a Call Option) – Total premium paid or (Strike price of a Put Option – Stock closing price) – Total premium paid

- Maximum risk: Limited, total premium paid

Please Enter Email

COMMENT (0)