Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Not every investor needs the same demat account. Your choice depends on where you live, how much you invest, whether you need to move funds abroad, and whether you want a lower-cost basic account or a more flexible setup.

For example, a resident Indian may use a regular demat account, while an NRI may need a repatriable or non-repatriable account. A small investor may prefer a Basic Services Demat Account (BSDA), while a company or trust may need a separate entity account.

This article explains the main types of demat accounts in India, their uses, charges, and key points to compare before choosing one.

A demat account stores securities in electronic form. These may include shares, ETFs, bonds, mutual fund units and other eligible securities.

You do not receive physical share certificates when you buy listed shares. Instead, the securities are credited to your demat account after settlement.

According to SEBI’s investor education material, investors cannot open an account directly with NSDL or CDSL. They need to open it through a registered Depository Participant, or DP.

A demat account makes investing easier and safer. It removes the need to handle paper certificates, reduces the risk of loss or forgery, and allows faster transfer of securities.

It also makes corporate actions smoother. Bonus shares, splits and similar benefits can be credited directly to the investor’s account.

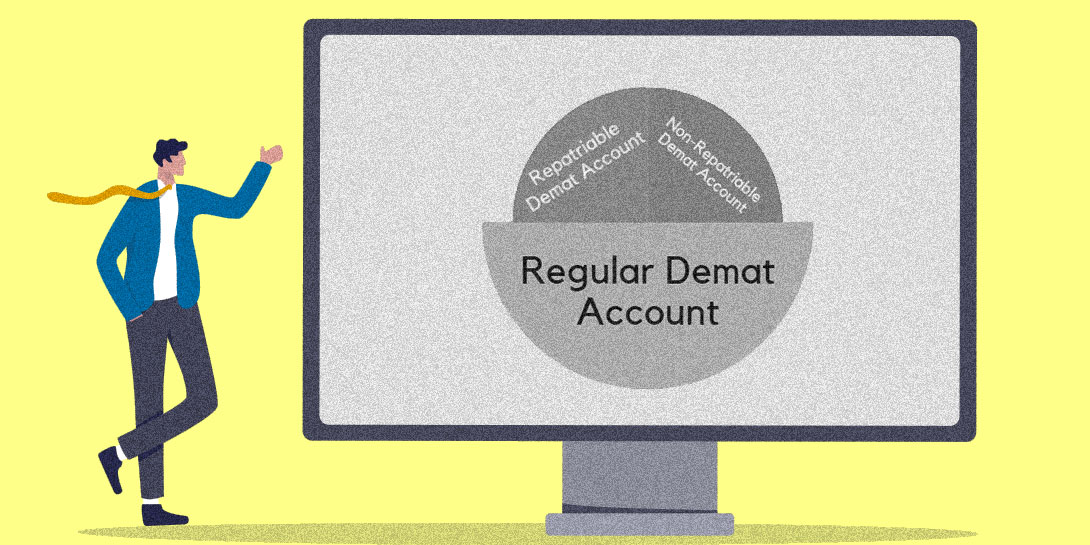

These three accounts have different roles.

For equity market investing, the three usually work together.

Investors do not have the same needs. A beginner with a small portfolio may want low maintenance charges. An NRI may need to follow FEMA and repatriation rules. A business entity may need an account in the organisation’s name.

That is why India has different demat account options for residents, NRIs, small investors and entities.

Demat accounts are designed for different investor needs, based on residency status and the type of securities held.

A regular demat account is meant for resident Indian individuals. It is the most common account used for buying, selling and holding securities in India.

It can usually be linked with a bank account and a trading account. There is no fixed upper limit on the value of securities you may hold, subject to applicable rules and broker policies.

Charges may include account-opening charges, annual maintenance charges, brokerage, DP charges, and transaction-related charges. Investors should compare the tariff before opening the account.

A basic services demat account is designed for small investors who do not hold a large portfolio. SEBI introduced BSDA to support financial inclusion and reduce demat account costs for eligible retail investors.

Earlier, the BSDA holding limit was ₹2 lakh. As per SEBI’s 2024 circular, this limit has been revised to ₹10 lakh for a single eligible individual. No annual maintenance charge applies for holdings up to ₹4 lakh, while holdings above ₹4 lakh and up to ₹10 lakh attract a capped AMC of ₹100.

An investor can have only one BSDA across all depositories. The account should be the sole or first holder account.

BSDA may suit long-term investors who buy and hold securities. However, active traders may prefer a regular account if they need wider service flexibility.

NRIs can open demat accounts in India. However, they must choose the correct account type based on whether the investment is repatriable or non-repatriable.

NSDL states that an NRI must mention the account type and subtype, such as repatriable or non-repatriable, while opening a depository account.

A repatriable demat account is linked to an NRE bank account. It is used when the investor wants to transfer eligible funds abroad.

This account is generally used for investments made through funds that can be repatriated, subject to RBI, FEMA and tax rules.

A non-repatriable demat account is linked to an NRO bank account. It is used for income earned in India, such as rent, dividends or sale proceeds.

RBI states that NRIs and PIOs may remit up to USD 1 million per financial year from NRO balances or eligible asset sale proceeds, subject to conditions and documentation.

Some investors need accounts for legal or ownership reasons. These accounts are opened based on the applicant’s structure and documents.

A corporate demat account is opened by companies, LLPs and other registered entities. It may be used to hold securities in the entity’s name.

A joint demat account can be opened by more than one holder. The first holder is usually treated as the primary holder, while the other holders are secondary holders.

Trusts and partnership firms can also open demat accounts. They need legal documents, PAN, authorised signatory details and other papers required by the DP.

An HUF demat account can also be opened in the name of the Karta of the HUF, subject to the applicable documentation and KYC requirements.

Choosing the right demat account is not only about charges. You should also look at platform quality, service, safety and how well the account fits your investing style.

Some brokers may offer free account opening, while others may charge a fee. The annual maintenance charge is a recurring cost, so it should be checked before applying.

If your portfolio is small, a BSDA may reduce your cost.

Brokerage is charged on trades, while DP charges may apply when securities are debited from the demat account. You should also check transaction charges, call and trade fees, pledge charges and other service costs.

A smooth digital process saves time. Look for online KYC, quick document upload, video verification and digital signing.

The app or web platform should be simple, stable and fast. It should allow easy order placement, portfolio review, charts and account tracking.

New investors often need market updates, reports and learning material. A broker with good research and simple education support can make decision-making easier.

Support matters when there are account, order, pledge, settlement or document issues. Check whether the broker offers phone, chat, email or branch support.

Choose an SEBI-registered broker or DP linked with NSDL or CDSL. A trusted brand with clear processes can reduce service-related concerns.

If you are a beginner or a student, you may start with a simple account and low charges. There is no fixed demat account age limit for adults, but minors need a guardian. So, if you are wondering, “Can a student open a demat account?” The answer is yes, if KYC and age rules are met.

If you are an NRI, choose the account based on repatriation needs. If you are an active trader, compare brokerage fees, platform quality, and DP charges. If you invest occasionally, a BSDA may be enough.

The right demat account depends on your investor profile. A regular demat account suits most resident Indians. A BSDA may suit small investors who want lower maintenance costs. NRIs should choose between repatriable and non-repatriable accounts based on fund movement needs. Entities, HUFs, trusts and partnerships need accounts that match their legal structure.

Before opening an account, compare charges, platform experience, service quality, research support and regulatory safety.

The main types are regular Demat accounts, BSDA accounts, NRI repatriable accounts, NRI non-repatriable accounts, joint accounts, and entity-based accounts.

A regular account is suitable for general investing. A BSDA is meant for eligible small investors and offers a lower AMC based on holding value.

Yes, NRIs can open demat accounts in India through a DP and must select the right NRI account type.

A repatriable account is linked to an NRE account and allows eligible funds to be transferred abroad. A non-repatriable account is linked to an NRO account and used for income from India.

It can be useful for beginners with a small portfolio, as maintenance charges may be lower.

Yes, you can have more than one demat account. However, you can have only one BSDA.

Aadhaar-based eKYC may make onboarding easier. However, the exact process depends on the broker, the DP, and the current KYC rules.

The account may remain open, but you should check charges, KYC status and statement alerts. Some service restrictions may apply if KYC is incomplete.

Submit a closure request to your DP after clearing dues and transferring or closing all holdings.

Yes, if you meet the BSDA conditions. The DP may also review eligibility based on holding value.

You should inform your DP and update your resident status. You may need to convert or open the correct NRI demat account.

SEBI has revised nomination rules to make the process easier. Investors should add or update nominations to support the smooth transmission of assets.

Yes, brokerage is charged for executing trades. DP charges are linked to demat account services, commonly when securities are debited from the account.

Understand silver trading, contract types, pricing factors, risks and expiry rules.

Additional Exposure Margin increases capital requirements for concentrated F&O securities.

Learn the essential F&O trading rules every beginner should understand before trading.

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App