Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Tax payments are likely to increase for those trading in stock market starting April 1, 2022. In the Union Budget 2022-23, the government has extended the scope of bonus stripping, which till now applied only to mutual funds, to stocks. That is likely to affect high-net-worth individuals, hedge funds, large overseas institutional investors and family offices.

Bonus stripping is a way by which investors would buy or sell shares or mutual funds in a manner in which they could adjust short-term capital loss against capital gains.

To illustrate with an example, an investor would purchase shares of a company that is about to issue bonus shares. They would buy the shares before the record date but after the company announces bonus shares.

After the record date, the company’s share price would adjust according to the bonus share issue. After adjusting the share price on exchanges, the investor would sell the original shares and book their loss.

Usually, the Income Tax Department uses the first-in, first-out approach to allow investors to book profit or loss. What happens here is two things – the short-term loss that the investor incurs post selling the original shares will be used to set off other capital gains. Moreover, after one year, the investor can pay a long-term capital gain of just 10% on the tax by selling the bonus shares. Let us understand this with an example:

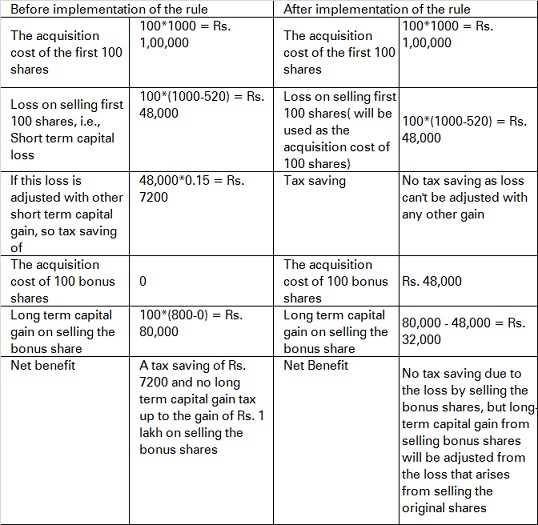

Suppose a company announced a 1:1 bonus and kept the record date as 10th Jan, 21. Suppose you purchased 100 shares @ Rs. 1000 on 1st Jan, 21 and post bonus stock price falls to Rs.500 and you received 100 more shares as a bonus. If you have sold 100 shares on 21st Jan @ Rs. 520 and remaining 100 shares on 30th Jan 2022 @ 800. The table below explains the tax liability in both scenarios, i.e., before implementing this rule and post-implementation.

Also Read: What is Long Term Capital Gain?

The new bonus stripping law does not allow this. Under the law, losses on bonus shares will be ignored for tax calculation purposes. However, the same loss can be treated as an acquisition cost for the bonus shares.

Please note that such loss can be ignored if an investor buys the shares within 3 months before the record date and sells the original shares within 9 months after the record date.

Investors who were earlier using bonus stripping as a tax planning tool will no longer do the same. They will only be able to use losses as acquisition costs when they sell bonus shares, thereby limiting the tax they can reduce. Such investors using bonus stripping for tax planning purposes will have to relook at their strategy.

Gold can react to inflation data, while crude oil may jump after an inventory report or geopolitical disruption.

Understand how crude oil trading works on MCX and also learn about contract sizes, expiry, trading hours, global benchmarks, price drivers and risks before you trade.

Learn how to calculate the break-even point in commodity trading by factoring in brokerage, taxes, and other charges

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App