Invest

Invest

Learning Modules Hide

Hide

- Chapter 1:Introduction to Mutual Funds

- Chapter 2: Advantages of Mutual Funds

- Chapter 3 : Regulation and Structure of Mutual Funds

- Chapter 4 : Mutual Fund Concepts : Part 1

- Chapter 5 : Mutual Fund Concepts : Part 2

- Chapter 6 : Types of Mutual Funds

- Chapter 7 : Basics of Debt Mutual Funds (Part 1)

- Chapter 8 Basics of Debt Mutual Funds: Part 2

- Chapter 9 : Duration and Credit Ratings in Debt Mutual Funds

- Chapter 10 : Types of Debt Mutual Funds

- Chapter 11 : Exchange Traded Funds: Part 1

- Chapter 12 : Exchange Traded Funds - Part 2

- Chapter 13 : Types of Mutual Fund Schemes

- Chapter 14 : Mutual Fund Investment Choices

- Chapter 15 : How to Choose Right Mutual Fund Scheme

- Chapter 1: Decoding the Mutual Fund Factsheet

- Chapter 2: Equity Mutual Funds – Evaluation-Part 1

- Chapter 3: Equity Mutual Funds – Evaluation (Part 2)

- Chapter 4: Equity Mutual Funds – Evaluation (Part 3)

- Chapter 5: How to Choose the Right Debt Mutual Fund

- Chapter 6: Mutual Fund Investment Choices – Switch and STP

- Chapter 7: Mutual Fund Investment Choices – SWP and TIP

- Chapter 8 - Mutual Fund Portfolio Management

- Chapter 9 Mutual Fund Return Calculations (Part 1)

- Chapter 10 Mutual Fund Return Calculations (Part 2)

Chapter 1: Introduction to Mutual Funds

Ritika produces ad films for a living. Driven and hard-working, she draws a good salary and diligently saves a part of it each month. However, the savings account she parks her money in pays very little interest. With the cost of living on the rise, Ritika worries that a savings bank account isn't enough.

She’s right!

Ritika already works hard for her money. What Ritika needs is for the money to work hard for her. One of the simplest ways to make that happen is by investing in mutual funds.

Mutual Funds in India: The backstory

India’s first mutual fund

The story of the mutual fund in India begins with forming of the Unit Trust of India (UTI) in 1963. Brought into being by an Act of Parliament, UTI was set up and controlled by the Reserve Bank of India (RBI) until 1978. That year, the Industrial Development Bank of India (IDBI) replaced the RBI as the UTI regulator and administrative authority.

The first mutual fund scheme launched by UTI was Unit Scheme 1964 (US 64). By the end of 1988, the total market value of the UTI investments amounted to Rs 6,700 crore.

The emergence of non-UTI mutual funds

In June 1987, the State Bank of India (SBI) launched the first non-UTI mutual fund. Between 1987 and 1992, five other public sector banks set up mutual funds of their own:

- Canbank in December 1987

- Punjab National Bank in August 1989

- Indian Bank in November 1989

- Bank of India in June 1990

- Bank of Baroda in October 1992

The Life Insurance Corporation of India (LIC) launched its mutual fund in June 1989. The General Insurance Corporation of India (GIC) followed suit in December 1990.

By 1993, the market value of investments in the mutual fund sector had ballooned to Rs 47,004 crore.

Rise of private sector mutual funds

The first private sector mutual fund was launched in 1993. The fund house that set it up—Kothari Pioneer—has since merged with Franklin Templeton.

That same year, the first Mutual Fund Regulations came into being. These regulated all mutual funds except those registered under UTI. The 1993 SEBI (Mutual Fund) Regulations were later replaced by more comprehensive and revised Mutual Fund Regulations in 1996.

|

Did you know? The mutual fund sector still functions under the SEBI (Mutual Fund) Regulations of 1996 but is amended from time to time. |

The entry of the private sector led to rapid growth in India’s mutual fund sector. That’s because:

- New mutual fund houses were launched

- Foreign mutual funds arrived on the scene

- Mergers and acquisitions took place

By the end of January 2003, India had 33 mutual funds with total assets worth Rs 121,805 crore. Indian investors now had more fund houses to choose from.

Mutual funds today

The new millennium marked a period of growth and consolidation for the country’s mutual fund sector. In 2019–20, the industry had assets under management (AUM) worth around Rs 27 lakh crore.

Mutual funds remain very popular in India today. That’s because:

- The investment process is easy and quick

- The returns are good

- Investors don’t need any market expertise

Besides, there are so many options! As a mutual fund investor, you can choose from among 43 asset management companies (AMCs) which offer more than 1,700 schemes!

*Source: AMFI and SEBI website

Understanding Mutual Funds

Ever planned a family picnic? There are always a few resourceful individuals who volunteer to do the planning. They book the venue, arrange for food, organise the transport, and make the payments as they arise. Everyone else simply contributes their share of the cost.

This analogy of a family picnic could help in understanding the concept of mutual funds.

- A mutual fund is an investment vehicle that collects money from a large group of investors.

- Similarly, when organising the picnic, the contributions from your family members are pooled together. Here, your family members could represent the 'large group of investors'. The share that each person pays is their 'investment'.

- A professional fund manager or a fund management team decides how to use this pool of money. They allocate the investors’ money across different asset classes.

- One could compare the fund manager (or the fund management team) with those family members who organise the picnic. Of course, unlike your enthusiastic uncle, the fund manager charges a fee for the service provided.

How is the investors’ money allocated?

The fund manager follows the objectives of the mutual fund scheme while allocating the pooled investment. An expert fund manager knows how to allocate the funds to different securities to generate good returns.

How are the returns distributed among the investors?

The returns are distributed in proportion to the number of mutual fund units that each investor holds. However, before making any pay-out, the fund house deducts certain charges. That includes fund management fees and other costs associated with running the mutual fund.

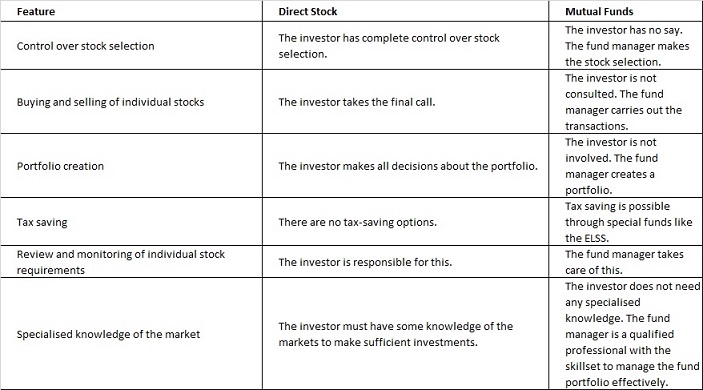

Mutual Fund investment vs direct investment in financial securities

Direct investment in financial securities like stocks and bonds can be rewarding if you:

a) are knowledgeable about the markets and

b) have the time to research and monitor securities.

Don’t have the financial knowledge or the time to monitor the markets? Mutual funds offer an easier way to invest. A professional fund manager takes care of the fund portfolio based on the mutual fund scheme's predefined objectives. The fund manager monitors the asset allocation of the fund and rebalances the portfolio when required. You, as the investor, can be rest assured that your money is in good hands.

Unsure about whether to invest in stocks directly or go for mutual funds? Check the differences between the two modes of investment in the table below before making your decision.

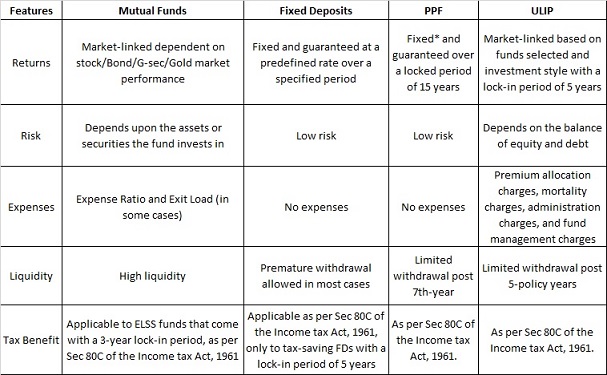

If you’re looking at how mutual funds stack up to other popular investment avenues, here’s how each one compares with the others. Knowing what each investment vehicle offers can help you make a smarter investment decision.

*Returns are fixed by the government of India every quarter

Summary

- A mutual fund is an investment vehicle that collects money from a large group of investors.

- The first mutual fund scheme in India was launched by UTI.

- Mutual funds in India are regulated and monitored by SEBI.

- You can choose from among 43 AMCs that offer more than 1,700 schemes.

- Expert fund managers professionally manage active mutual fund schemes.

- If you don't have the financial knowledge or the time to monitor the markets, mutual funds offer an easier way to invest.

Now that we have covered how mutual funds can be a good fit for your investment needs, we move on to the next chapter. In the next chapter, Advantages of Mutual Funds, we look into the many benefits of investing in mutual funds for your financial goals and lifestyle.

Disclaimer:

ICICI Securities Ltd. ( I-Sec). Registered office of I-Sec is at ICICI Securities Ltd. ICICI Venture House, Appasaheb Marathe Marg, Prabhadevi, Mumbai - 400 025, India, Tel No : 022 - 6807 7100.I-Sec acts as a Composite Corporate agent having registration number –CA0113. PFRDA registration numbers: POP no -05092018. AMFI Regn. No.: ARN-0845. We are distributors for Mutual funds and National Pension Scheme (NPS). Mutual Fund Investments are subject to market risks, read all scheme related documents carefully. Please note, Mutual Fund and NPS related services are not Exchange traded products and I-Sec is just acting as distributor to solicit these products. Please note, Insurance related services are not Exchange traded products and I-Sec is acting as a corporate agent to solicit these products. All disputes with respect to the distribution activity, would not have access to Exchange investor redressal forum or Arbitration mechanism. The contents herein above shall not be considered as an invitation or persuasion to trade or invest. I-Sec and affiliates accept no liabilities for any loss or damage of any kind arising out of any actions taken in reliance thereon. Investments in securities market are subject to market risks, read all the related documents carefully before investing. The contents herein mentioned are solely for informational and educational purpose.

COMMENT (0)