Uptick in sugar prices to offset lower sugar recovery…

About The Stock

Triveni Engineering (TEL) is one of the largest sugar companies in India with sugar crushing capacity of 61,000 TCD, distillery capacity of 660 KLD & co-generation power of 104.5 MW. It also has power transmission & waste water management business contributing 10% to revenues.

The company is increasing its distillery capacity from the current 22 crore litre per annum to 32 crore litre per annum by FY25 to utilise B-heavy, grain & sugarcane juice route to produce ethanol

Q4FY23 Results

Posted 47.8% sales growth led by strong sugar, ethanol sales.

Sales were up 47.8% YoY with 108.6% growth in distillery sales

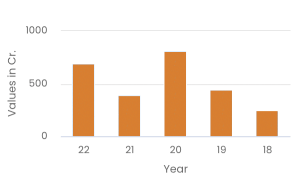

EBITDA was at ₹ 263.3 crore, up 50.7% YoY, with margins at 16.6%

PAT was at ₹ 190.3 crore, up 74.3% YoY aided by lower interest costs

Sugar company Triveni Engineering & Industries announced Q3FY24 & 9MFY24 results:

Net turnover declined by 10.4% and 2.9% respectively in Q3FY24 and 9MFY24:

Overall sugar sales volumes (including exports) were lower by 17.6% and 13.0% in Q3 and 9MFY24 respectively as compared to corresponding periods in the previous year which included substantial exports. It led to lower turnover in the Sugar business by 9.2% and 8.2% in Q3FY24 and 9MFY24 respectively, despite ~6% higher blended realisations both in the quarter and the nine-month period.

Alcohol business turnover (net of excise duty) increased by 7.6% and 16.0% in Q3 and 9MFY24 respectively, over the corresponding period last year, due to higher sales volumes driven by operational efficiencies and increased activities in Indian Made Indian Liquor (IMIL).

The Power Transmission business reported robust revenue growth of 17.5% and 33.9% in Q3 and 9MFY24 over the previous year driven by capacity augmentation (including exports)

Water business reported lower turnover of 48.8% and 24.2% in Q3 and 9MFY24 due to slower execution in some projects.

Profit before tax and exceptional items (PBT) declined 8.4% in Q3FY24 and was flat in 9MFY24 to Rs 182.1 crore and Rs 312.3 crore respectively.

Sugar business reported higher profitability due to higher sugar realisation prices offsetting the impact of lower sales volumes and increase in costs due to revision in State Advised Price (SAP) of sugarcane.

PTB also reported higher profitability commensurate with higher turnover.

Decline in the profitability of distillery operations is mainly due to a higher proportion of lower margin maize operations in substitution of FCI rice.

Segment profitability of the Water business during the current quarter is in line with the lower turnover whereas it has been able to maintain profitability during 9 months due to cost savings in various projects.

The gross debt on a standalone basis as of December 31, 2023, is Rs 514.5 crore as compared to Rs 389.1 crore as of December 31, 2022.

However, after considering surplus funds held as fixed deposit (FD) of Rs 369.0 crore, the net debt as of December 31, 2023, is at Rs 145.5 crore.

Standalone debt at the end of the quarter under review, comprises term loans of Rs 262.4 crore, almost all such loans are with interest subvention or at subsidized interest rates.

On a consolidated basis, the gross debt is at Rs 602.9 crore as of December 31, 2023, as compared to Rs 480 crore as of December 31, 2022, and the net debt as of December 31, 2023, is Rs 233.9 Crore.

Overall average cost of funds is at 5.25% during Q3FY24 as against 4.75% in the previous corresponding period.

Commenting on the Company’s financial performance, Dhruv M. Sawhney, Chairman, and Managing Director, Triveni Engineering & Industries, said: “Overall performance of the Company during the nine-month ended December 31, 2023, has been satisfactory, with healthy performance in Sugar and Power Transmission businesses in particular. There were challenges in the Alcohol business due to feedstock constraints and the profitability of the Water business was impacted due to the slow execution of some projects due to problems relating to the customers.

We are witnessing improved operational results in the Sugar business in the ongoing SS 2023-24 in terms of crush, recovery, and sugar realisation price over the previous year/season. The current estimates of lower production in SS 2023-24 and SS 2024-25 are likely to maintain firm sugar prices. The recent increase in sugarcane price by Rs 20 per quintal can be well absorbed by the prevailing sugar prices. A higher proportion of refined sugar production post-conversion of our Milak Narayanpur sugar unit to refinery and a higher quantum of pharmaceutical-grade sugar production at Sabitgarh augur well for sugar realisations for the Company. We continue to make judicious investments in our facilities to enhance crush rate, sugar quality, and efficiencies.

While there may be a significant shortfall in production in Maharashtra and Karnataka, Uttar Pradesh (UP) is estimated to show higher production. The recent weather conditions in UP of dense fog with no sunshine for a longer duration may have some impact on the yields and recoveries. Further, in view of restrictions to use Bheavy molasses and sugarcane juice to limit sugar sacrifice for ethanol production, sugar operations are largely being carried out with C-heavy molasses, which will lead to higher sugar production but can also have some impact on recoveries."

Invest

Invest