Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

When companies require large funding, they do so by issuing equity or raising debt. This is recorded in the cash flow statement. The portion of the net cash generated by a company over a certain time period that goes into funding the firm itself is called Cash Flow from Financing Activities (CFF). Borrowing and repayment of the debt, disbursement of dividends and equity repayments are all a part of Cash Flow from Financing Activities.

The cash flow statement is one of the three critical financial documents published by a company, which gives a detailed account of how the company is faring in terms of financial performance. They are:

There are 3 sections in a Cash Flow Statement:

1. Cash Flow from Operations (CFO): This section records all cash flows generated by the core business operations. Cash flows that directly deal with operating activities are accounts payable, accounts receivable, depreciation and amortisation, etc

2. Cash Flow from Investing Activities (CFI): As the name suggests, all cash flows generated or consumed in the buying and selling of capital assets are found in this section. Profits and losses arising from investments in fixed assets are found here.

3. Cash Flow from Financing Activities (CFF): This section essentially captures the flow of cash between the business and its investors, owners, and creditors. As mentioned earlier, here you can find the net funds that are used to finance the company.

Investors who wish to dive into further details about the company’s debt and equity structure can take a look at the ‘liabilities’ and ‘shareholders’ equity’ sections of the company’s balance sheet.

Cash Flow from Financing Activities umbrellas all cash flows that fund the core operations of a business. That is why all changes in the debt and equity accounts are found here. It is, thus, very important for investors and analysts alike to know what falls under this section of the Cash Flow Statement.

Cash Flow occurring through the following activities is clubbed under Cash Flow from Financing Activities:

Here is how cash flows from these activities will be treated in the CFF section:

Now that we know what is cash flow from financing activities, let us check the cash flow from financing activities formula.

Where:

CED = Cash inflow from issuance of debt/equity

CD = Cash disbursed as dividends

RP = Repurchase of debt/equity

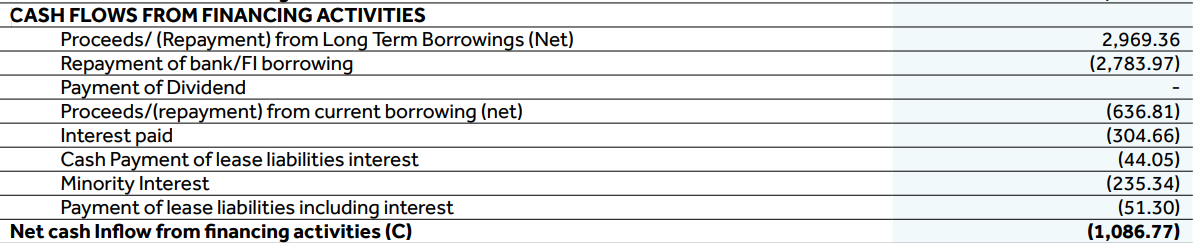

Given below is a snapshot of the CFF of a listed company on the BSE.

As you can see in the Cash Flow from Financing Activities section, the issuance a long-term of debt has been recorded as a positive cash flow (inflow). On the other hand, the payment of dividends, repayments of bank borrowings, interest and lease payments have all been recorded as negative cash flows (outflow).

Since the summation of all these recorded values is negative, it means that there was net cash outflow in the given period, and its major contributor was the repayment of bank borrowings.

Whenever a company shows tendencies to borrow, it may reflect positively in the Cash Flow from Financing, but it also means that it is not generating adequate cash flow to sustain its operations. Similarly, a hike in interest rate also raises the repayment amount. Hence investors must be vigilant about such things and have a keen eye for numbers and discrepancies.

On the flip side, if a company is buying back shares from the open market and then issuing dividends while showing unsatisfactory performance, then it is a likely red flag. This move can be a management strategy to bolster its share price and look more valuable although it is not. These actions are not favourable for the company in the long term.

Major deviations from the normal cash flow trend should catch the attention of investors, who must then investigate further by diving deeper. While analysing a Cash Flow Statement, equal attention must be given to all three sections and not just one section alone.

Disclaimer: ICICI Securities Ltd. (I-Sec). Registered office of I-Sec is at ICICI Securities Ltd. - ICICI Venture House, Appasaheb Marathe Marg, Prabhadevi, Mumbai - 400 025, India, Tel No : 022 - 6807 7100. I-Sec is a Member of National Stock Exchange of India Ltd (Member Code :07730), BSE Ltd (Member Code :103) and Member of Multi Commodity Exchange of India Ltd. (Member Code: 56250) and having SEBI registration no. INZ000183631. AMFI Regn. No.: ARN-0845. We are distributors for Mutual funds. Mutual Fund Investments are subject to market risks, read all scheme related documents carefully. Name of the Compliance officer (broking): Ms. Mamta Shetty, Contact number: 022-40701022, E-mail address: complianceofficer@icicisecurities.com. Investments in securities markets are subject to market risks, read all the related documents carefully before investing. The contents herein above shall not be considered as an invitation or persuasion to trade or invest. I-Sec and affiliates accept no liabilities for any loss or damage of any kind arising out of any actions taken in reliance thereon. The contents herein above are solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments or any other product. Investors should consult their financial advisers whether the product is suitable for them before taking any decision. The contents herein mentioned are solely for informational and educational purpose.

From supply disruptions and weather events to geopolitical developments, commodity prices move on a wide range of forces.

Understand silver trading, contract types, pricing factors, risks and expiry rules.

Additional Exposure Margin increases capital requirements for concentrated F&O securities.

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App