Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Hedging essentially means limiting risk on any asset class or a portfolio. Similarly, the concept of Delta hedging emerges in options trading which essentially mean to offset the losses in Stock by corresponding gain in option or vice versa. Let me explain you the basic hedging with example and then we can get into the delta hedging in depth:

Let’s say you have bought some quantity of shares of ITC for long term investing in your portfolio. Now you want to limit the downside risk for these shares, thus you can simply BUY PUT with an appropriate DELTA to hedge your position by giving net debit. In case if the stock doesn’t move much in either direction, you tend to lose the premium paid on PUT option due to daily erosion of time value. On the other hand you haven’t made enough profit on stocks. To overcome such scenario, an investor can make use of Delta Hedging by shorting CALL option to protect its investment from movements in either direction. If the price doesn’t move at all then the CALL option loses it time value and the investor tends to make profit from call options while remaining no-profit/no-loss on the underlying stock.

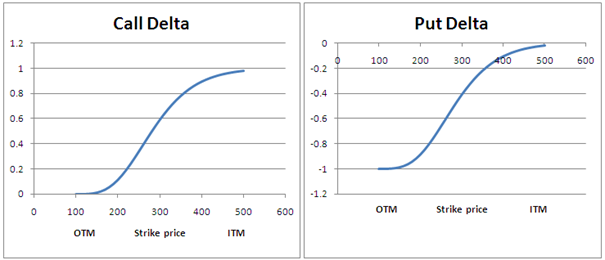

So what is DELTA? It is one of the options GREEK that tells us the change in the price of an option for a unit change in price of an underlying. In layman terms, for every Rs.1 change in stock price, by how much the price of the option changes? is what an option trader aims to find out to limit the risk on its position. Once you have a good grasp of delta, you can manage your investments wisely and make profit by hedging it to make a side income. The delta is calculated using the Black-Scholes-Merton formula which is a complex model designed by Fischer Black and then it was further developed by Myron Scholes and Robert Merton. Their valuable contribution was recognized by Nobel committee and has awarded them with Nobel prize in 1997 for their work. I will not get into the calculation detail of BSM model as it’s a very big topic in itself which I can take up later in another blog. For the sake of this article all we need to understand now is that Delta ranges between Zero to One (0 to +1) for CALL side, moving from OTM to ITM of an options and (-1 to 0) on PUT side, moving from OTM to ITM option. The Below graph details the Strike price with moneyness on X-axis and the corresponding delta value on Y-axis.

Assuming that you already know the moneyness of the option concept (ITM, ATM and OTM) we can proceed further to understand the details of the Delta hedging in depth.

Suppose you have sold the ITC ATM CALL option. From the above graph you can observe that the ATM call option has a delta of 0.5. So you are net short on 0.5 delta and therefore the position will appear as follows:

Stock: ITC

ITC Lot Size: 3200

Current Market Price of the Stock: 200

Option Price of ATM CALL: Rs.10

So when you sell ATM strike of 200 with 0.5 Delta, this mean you are SHORT on 1600 shares (0.5 x 3200) in CALL options. In order to hedge, you will need to BUY 1600 shares of Stocks to make it Delta Neutral. Once you do that, you are perfectly hedged but in real life there is no such thing as perfect hedge because market keeps changing continuously and so will your hedged position. With this changing market conditions you will wonder what will happen to your hedged position if the stock moves up or below by one rupee? The answer lies in Delta. Because you have shorted ATM Call options, the one rupee gain in Stock price will increase the CALL option price by Rs 0.5. In other words, if the Stock price increases to Rs. 201, then the price of the option will go to Rs.10.5 or if the Stock price drops to Rs.199 then the price of the options will drop down to Rs.9.5 assuming no changes in other Greek parameters.

The P&L calculation for every change in price is given in below table: you can download the spreadsheet from here in case you want to check for various scenarios. So, if you keep Buying/Selling stocks accordingly as per column G, then you would have dynamically hedged your portfolio. But in practical this is close to impossible for a trader who does this manually. For this you either need to develop software which does this for you or try to buy a tool readily available from some vendor who provides such dynamic hedging feature. For a retail trader, it is quiet difficult to make profit from this strategy because the brokerage and taxes will eat up good chunk of your profits. Thus to keep your cost to minimum, you can take advantage of ICICIdirect Prime plan where you are only charged Rs.7 per order for options. And if you are an advanced trader who only trades in FUTURES and hedges using options, then you can take advantage of the ICICIdirect Prime plan which also provides you with 0.05% brokerage on trading in FUTURE.

|

A |

B |

C |

D |

E |

F |

G |

H |

I |

|

Current Market Price of Stock |

Delta of Option |

CALL option Price w.r.t change in Delta |

ITC Stock P&L |

Call P&L: lot size = 3200 |

Combined P&L |

Action to take: Buy/Sell of Stocks Qty |

Initial Stock Qty |

Stock Qty after Adjustments |

|

197 |

0.46 |

8.53 |

-4704 |

4704 |

0 |

-64 |

1536 |

1472 |

|

198 |

0.48 |

9.01 |

-3168 |

3168 |

0 |

-32 |

1568 |

1536 |

|

199 |

0.49 |

9.5 |

-1600 |

1600 |

0 |

-32 |

1600 |

1568 |

|

200 |

0.5 |

10 |

0 |

0 |

0 |

None |

1600 |

|

|

201 |

0.51 |

10.5 |

1600 |

-1600 |

0 |

32 |

1600 |

1632 |

|

202 |

0.52 |

11.01 |

3232 |

-3232 |

0 |

32 |

1632 |

1664 |

|

203 |

0.54 |

11.53 |

4896 |

-4896 |

0 |

64 |

1664 |

1728 |

|

202 |

0.52 |

10.99 |

3168 |

-3168 |

0 |

-64 |

1728 |

1664 |

Understand silver trading, contract types, pricing factors, risks and expiry rules.

Additional Exposure Margin increases capital requirements for concentrated F&O securities.

Learn the essential F&O trading rules every beginner should understand before trading.

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App