Invest

Invest

Furniture-Furnishing Paints company Cera Sanitaryware announced Q3FY24 & 9MFY24 results:

Standalone Q3FY24:

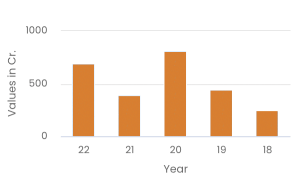

- Revenue from Operations (Net of Taxes): Rs 4,367 million in Q3FY24 compared to Rs 4,557 million in Q3FY23, showing a decrease of 4.2%.

- EBITDA (Excluding Other Income): Rs 594 million in Q3FY24 compared to Rs 729 million in Q3FY23, indicating a decrease of 18.5%.

- EBITDA Margin: 13.6% in Q3FY24 compared to 16.0% in Q3FY23, reflecting a decrease of 240 basis points.

- Profit After Tax (PAT): Rs 509 million in Q3FY24 compared to Rs 564 million in Q3FY23, representing a decrease of 9.7%.

- PAT Margin: 11.7% in Q3FY24 compared to 12.4% in Q3FY23, indicating a decrease of 70 basis points.

- EPS Diluted: Rs 39.12 in Q3FY24 compared to Rs 43.34 in Q3FY23, showing a decrease of 9.7%.

Standalone 9MFY24:

- Revenue from Operations (Net of Taxes): Rs 13,246 million for 9MFY24 compared to Rs 12,656 million for 9MFY23, indicating a growth of 4.7%.

- EBITDA (Excluding Other Income): Rs 2,022 million for 9MFY24 compared to Rs 2,001 million for 9MFY23, showing a slight increase of 1.1%.

- EBITDA Margin: 15.3% for 9MFY24 compared to 15.8% for 9MFY23, reflecting a decrease of 50 basis points.

- Profit After Tax (PAT): Rs 1,641 million for 9MFY24 compared to Rs 1,467 million for 9MFY23, indicating a growth of 11.9%.

- PAT Margin: 12.4% for 9MFY24 compared to 11.6% for 9MFY23, showing an increase of 80 basis points.

- EPS Diluted: Rs 126.21 for 9MFY24 compared to Rs 112.81 for 9MFY23, representing a growth of 11.9%.

Commenting on the performance, Vikram Somany, Chairman & Managing Director, said, “Revenues in Q3FY24 decreased by 4.2% YoY, totaling Rs 4,367 million, while profit after tax experienced a 9.7% YoY decline, amounting to Rs. 509 million. Our sanitaryware and faucet ware divisions, contributing 52% and 36% to our Q3FY24 revenue, witnessed a decrease of 8% and increase of 5%, respectively.

This quarter’s performance was marked by a challenging market-led slowdown characterized by subdued demand across key markets. Despite these challenges, the Company remains confident in its strong fundamentals and maintains optimism in its overall growth outlook. Our commitment to strategic initiatives, particularly the focus on premiumization, played a pivotal role in navigating this period. We remain dedicated to optimizing our operations and fostering growth in the face of varying market conditions.

Our recently commissioned brownfield faucetware capacity, operational since the previous quarter, is demonstrating positive performance.

A recent notable achievement was the acquisition of a substantial portion of land for our upcoming state-of-the-art sanitaryware facility in Gujarat. We are enthusiastic about this upcoming addition to our infrastructure, emphasizing our commitment to broadening our portfolio of value-added products. These products will be exclusively manufactured within our facility, leveraging advanced technical capabilities and adhering to rigorous quality standards. While we will continue to outsource low-end products, typically those that do not require specialized expertise, this strategic approach ensures that our commitment to excellence remains focused on in-house production for more intricate and sophisticated offerings.

As we move forward, Cera is strategically positioned to capitalize on its strengths, ensuring they not only navigate macro-led challenges but also foster sustained growth for all stakeholders.”