Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Capital gains means, any gain arising on the sale of capital assets such as real estate, equity or equity oriented products. Here we will discuss about the long term capital gain arising on sale of equity and equity oriented funds. Now, investment in shares or equity oriented mutual funds can be done for a short term or long term. Short term means investing for a period of upto 12 months and long term means investing for a period of more than 12 months.

Suppose if you bought a share on Jan 1, 2017 at Rs 100 and sold on Dec 1, 2017 at Rs.130. This Rs. 30 gain will be short term capital gain. Now if suppose you sell the shares on Jan 15, 2018, then this will be treated as long term capital gain.

Short Term Capital Gain Tax- Any profit or gain arising from stock investment is less than 12 months termed as short-term Capital gains. Short term capital gain tax is taxed at flat rate of 15%.

Long term Capital Gain Tax- Any profit or gain arising from stock investment is considered long term capital gains, if the holding period is more than 1year. Long term capital gains up to Rs 10000 from investment in a financial year is exempted from tax. Any gain above RS 100000 is taxed at 10%. Until FY 2017-18, a LTCG tax on sale of stocks was zero. In the Union budget of FY2018-19, a grandfather clause was introduced. According to this clause, all the stocks sold after February 1, 2018 the acquisition cost for the computation of capital gains would be considered as higher than the actual purchase price or the highest price quoted on stock exchange as on January 2018

Short term capital gain tax

Mr A bought 100 shares of Larsen & Toubro ltd at Rs 950 per share on 8th June2020 and sold the same 100 shares of Larsen & Toubro at Rs 1500 per share on 15th February 2021 within 1year (less than 12 months).

LARSEN AND TUBRO (INE018A01030), HOLDING PERIOD = 8 MONTHS 6 DAYS

|

Stock Name |

BUY VALUE |

SALE VALUE |

GAIN (SALE-BUY) VALUE |

|

LARSEN & TOUBRO |

95,000 |

1,50,000 |

55,000 |

Gain on Larsen & Toubro is Rs. 55,000/-.

Short term capital gain tax = 55000 X15% = 8250.

Long term capital gain tax

Mr P bought 200 shares of Titan Ltd. At Rs 820 per share on 27th November 2017 and sold the same 200 shares of Titan at Rs 1700 per share on 1st July 2021

TITAN (INE280A01028), HOLDING PERIOD= 3 YEARS 8 MONTHS

|

Stock Name |

BUY VALUE |

SALEVALUE |

GAIN (SALE- BUY) VALUE |

|

TITAN |

164000 |

340000 |

176000 |

Long Term Capital Gain = 176000 (Up to Rs 100000 is not taxed as per the provision)

Long term capital Gain Tax= (176000-100000) = 76000 X 10% = 7600

Any Unadjusted losses can be carried forward up to 8 years. However, if there is any capital loss, then file it before due date to carry forward the loss and then set off from the capital gains arising in future. Short term capital loss can be carried forward up to 8 years and can be set off against short term capital gain and long-term capital gain before taxation. Long term capital loss can be carried forward for up to 8 years and can be set off against long term capital gains only before taxation.

Intraday-day trading (speculative business income)- If the shares are bought and sold regularly in a short duration then this is not considered to be under capital gains but under speculative business income as per income tax section 43(5). The gain from this type of income is taxed under business income and is taxed as per the assesses tax slab rate.

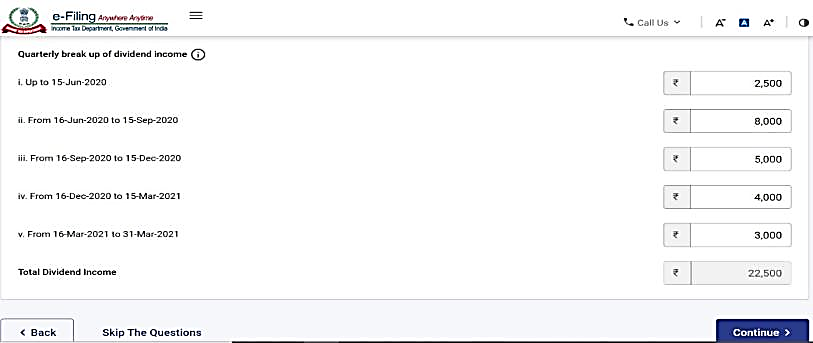

As per Finance Act 2020 shareholders will have to pay the tax on dividend income as per their tax slabs at and additional TDS would be charged at 10% if the dividend from any company received exceeds Rs 5000.

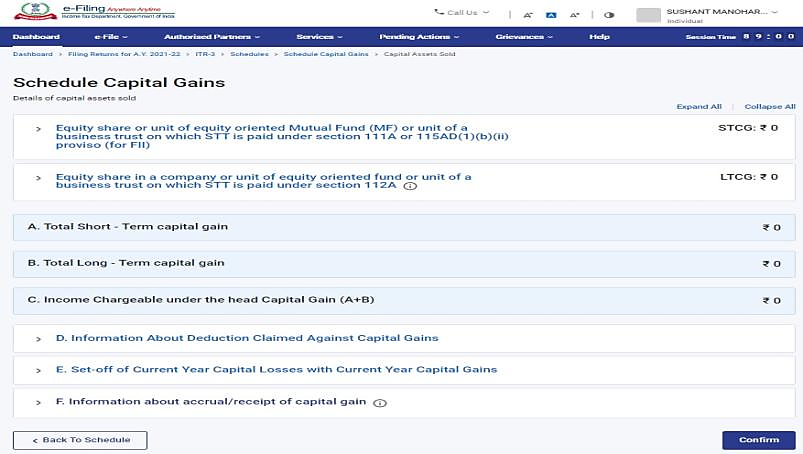

You need to visit Income Tax website to file your tax.

ITR-3 for Individuals and HUFs having income from profits and gains of business or Profession

ITR-4 for Individuals, HUFs and Firms (other than LLP) who are eligible to opt for “Presumptive taxation scheme”

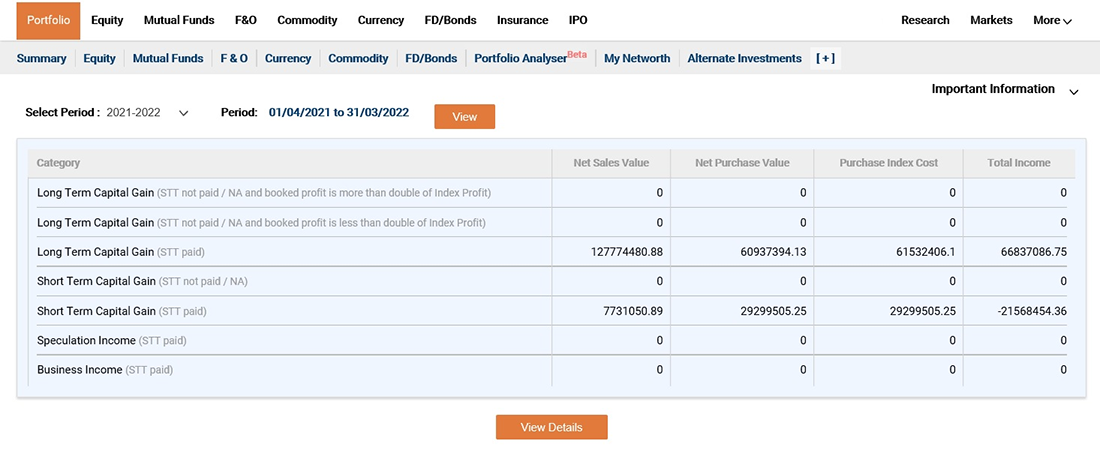

LOGIN TO ICICIDIRECT ACCOUNT > PROFOLIO> Capital Gain (Equity section)> View Caital Gain

Choose the right period and then click on view details and there on download at the top right to get the file in .als or .csv format, and Save the same to get the file.

Long term Capital Gain= Sale value - Cost of acquisition

Sale value means the consideration received on the sale of equity share.

The concept of Grandfathering means that any gain calculated upto 31st Jan 2018 i.e. taking the highest price of the stock as on Jan 31, 2018, will not be chargeable to tax. This price as on Jan 31, 2018 is the fair market value as on Jan 31, 2018.

Gains on stock after Jan 31, 2018, will be chargeable to tax of 10% provided the shares are sold on or after April 1, 2018. Please note, If the shares are sold on or upto March 31, 2018, any long term capital gain will be exempt from tax.

Now, there are scenarios to determine the cost of acquisition.

Scenario 1: First check if the Sale value is higher than the fair value as on Jan 31, 2018. If yes, then the higher of fair market value as on Jan 31, 2018 and actual cost of acquisition will be treated as the Cost of acquisition.

Let’s assume:

Shares acquired- 1st of January, 2017

Actual Acquisition Price =Rs. 100,

Fair market value as on Jan 31, 2018= Rs. 200 (This is the highest trading price as on Jan 31, 2018)

Sale value on 1st of April, 2018 = Rs. 250.

Here, since the sale value as on 1st April 2018 is higher than the FMV as on 31st Jan, the cost of acquisition will be higher of 200 and 100, which comes to Rs.200.

In this case, the LTCG will be 250-200= Rs.50

Scenario 2: If the Sale value is lower than the fair value as on Jan 31, 2018. If yes, then cost of acquisition will be the higher of sale value and actual cost of acquisition.

Let’s assume:

Shares acquired- 1st of January, 2017

Actual Acquisition Price =Rs. 100

Fair market value as on Jan 31, 2018= Rs. 200

Sale value on 1st of April, 2018 = Rs. 150.

Here, since the sale value as on 1st April 2018 is lower than the Fair market value as on 31st Jan, the cost of acquisition will be higher of sale value and actual cost of acquisition i.e. higher of 150 and 100, which is Rs.150 will be considered as the cost of acquisition

In this case, the LTCG will be 150-150= Rs.0

Scenario 3:

Let’s take another example in which, sale value is less than the actual cost of acquisition.

Shares acquired- 1st of January, 2017

Actual Acquisition Price =Rs. 100

Fair market value as on Jan 31, 2018= Rs. 200

Sale value on 1st of April, 2018 = Rs. 80.

In this case, the sale value is also lower than the fair market value as on Jan 31, 2018. Hence the cost of acquisition will be higher of actual cost of acquisition and the sale value, i.e. Rs 100 and Rs.80. Hence cost of acquisition will be Rs.100.

So there will be long term capital loss of Rs. 20 (Rs.80 minus Rs.100)

Will cost of acquisition be indexed for calculating Long term capital gains?

No, benefit of indexation of the cost of acquisition will be applicable for calculating long term capital gains tax.

What is Tax Loss Harvesting-

Tax-loss harvesting is the practice of selling a share that is incurring a loss, so that by realizing the loss, you can offset the same against realized gain for the same year and save on taxes. The security has to move out of the demat account by delivery sell transaction and the sold security is replaced by the same or a similar security.

When can client needs to take action for tax loss harvesting?

Client would need to make these transactions before March 31, 2022 to harvest losses for Financial Year 2021-22.

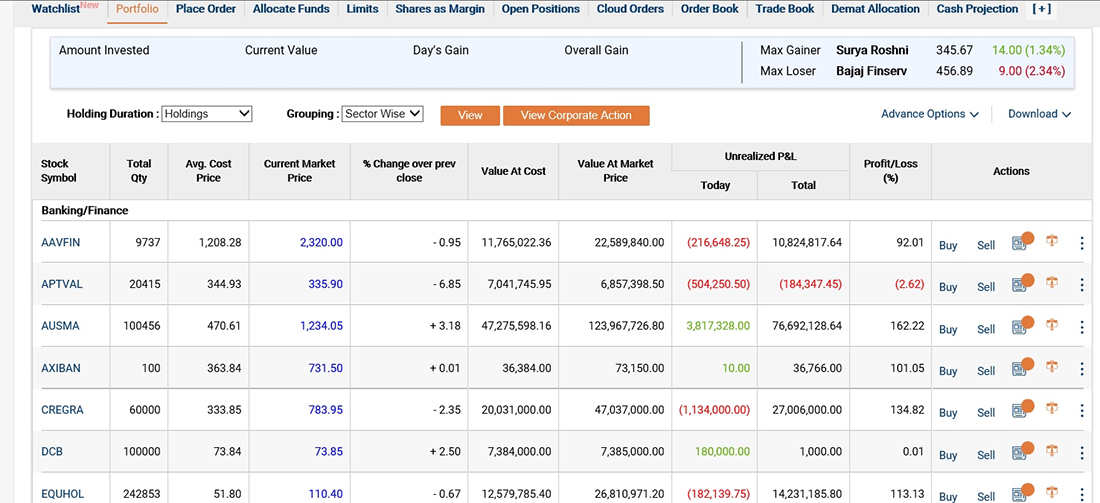

Where client can check unrealized capital gain in ICICIdirect ?

Client can check unrealized capital gain by logging in to ICICIdirect account and visiting the "Equity" section under "Portfolio".

Examples for Tax Loss Harvesting:-

1) Short Term Capital Gain

Assume that you have made a Short Term Capital Gain (STCG) of ₹1,00,000 this year. Client would have a 15% tax liability i.e. ₹15,000 on the same. Also assume that client is currently holding some stocks where client has a unrealized loss of ₹80,000. Client can sell these stocks and set off the loss of ₹80,000 against STCG of ₹1,00,000. Hence, client would only need to pay 15% tax on ₹20,000 which is ₹3,000, thereby saving ₹12,000

Once this Tax harvesting activity is completed, you can again buy the same stock or a similar scrip, maintaining optimal asset allocation and expected returns.

2) Long Term Capital Gain

Assume that client has made a Long Term Capital Gain (LTCG) of ₹3,00,000 this year. You would need to pay 10% tax on the (₹3,00,000 - ₹1,00,000*) = ₹2,00,000 i.e. ₹20,000. Also assume that client is currently holding some stocks where for more than 1 year and you have an unrealized loss of ₹1,50,000. Client can sell these stocks and set of the loss of ₹1,50,000 against LTCG of ₹2,00,000. Hence, client would only need to pay 10% tax on ₹50,000 which is ₹5,000, thereby saving ₹15,000

*First & ₹1,00,000 made in LTCG would be tax free and any gain above that would be taxed at & 10%.

While setting off losses in tax harvesting, you need to keep following points in mind

1. Long term capital losses can be set off only against long term capital gain.

2. Short term capital losses can be set off against short term capital gains or long term capital gains.

Note:

1) The tax liability explained here is a guideline, we suggest you to consult your tax advisor to understand the exact tax liabilities.

2) Please note that the amount given in the above examples are hypothetical and have no relevance to your portfolio. You may calculate the amount of STCG/ LTCG based on your portfolio.

Gold can react to inflation data, while crude oil may jump after an inventory report or geopolitical disruption.

Understand how crude oil trading works on MCX and also learn about contract sizes, expiry, trading hours, global benchmarks, price drivers and risks before you trade.

Learn how to calculate the break-even point in commodity trading by factoring in brokerage, taxes, and other charges

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App