Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

The Union Budget 2023 is round the corner and being the last such full-fledged exercise before the general elections next year, there is a heightened sense of expectation across stakeholders.

Indirect taxes are now subsumed by the GST (goods and services tax) and decisions on rates are taken by the GST council. Policy announcements on incentives and taxations for corporates have also been made outside the budget exercise. So, budgets have been more about allocations to various departments and government programmes in recent years. Therefore, much of the retail interest in the budget has centred around the occasional personal tax announcements made by the finance minister.

Given that there have been very few giveaways in the form of lower taxation over the past several budgets and most income sources (dividends, interest etc.) have been made fully taxable, it may be better for taxpayers to temper their expectations.

Even so, given the continuous requests from many quarters, there may yet be some announcements to give relief to the middle class.

In particular, three areas may receive attention. First is incentivising more people to opt for the new concessional tax regime – as it has few takers now – by making it more attractive. Second is the long-pending demand for increasing deductions under sections 80C, 80D and 80CCD, apart from lowering tax slab rates in the ‘with exemptions’ regime. Third is the talk around rationalisation of taxes across equity, debt and real estate in terms of capital gains taxes and holding periods.

Here is what taxpayers could expect from Budget 2023.

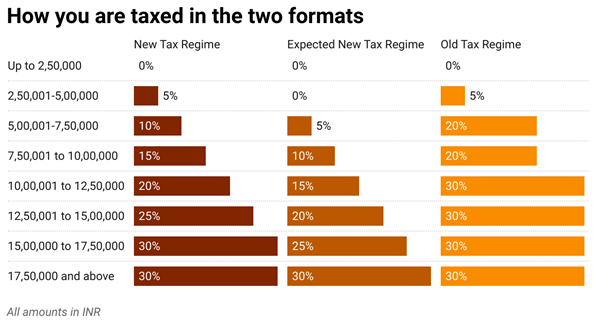

Current status: In Budget 2020, the government announced a parallel new tax regime to the existing one. The concessional tax regime came about on the thought process that taxpayers must eventually contend with fewer or no deductions and exemptions, in lieu of a simpler structure and lower slabs.

So, we had six slabs on taxes with rates starting from 5% on income from Rs 2.5 lakh to Rs 5 lakh. In slabs of Rs 2.5 lakh, the rates increased progressively and for income above Rs 15 lakh, it was 30%.

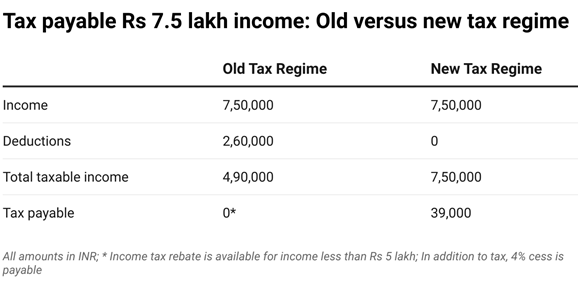

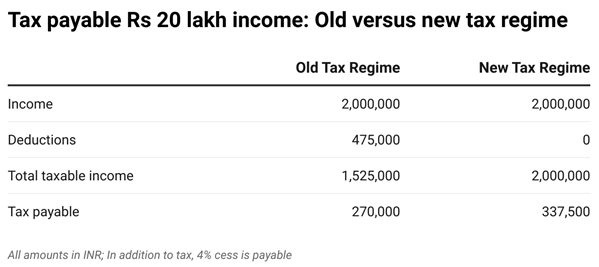

In India, where most of those filing returns earn much less than Rs 10 lakh, the old regime with deductions and exemptions worked very well even with small sums.

The following examples would make that clear that the new tax regime in the present form would not be successful in getting most taxpayers interested.

Expectations: There have only been an estimated 5 lakh tax filers who opted for the concessional regime. Most economists and officials in the finance ministry have aired their view in favour of tweaking the new tax regime to make it attractive to more taxpayers.

Two key changes may be expected in this regard. First, the minimum taxable income could be moved to Rs 5 lakh from the existing Rs 2.5 lakh. Then, in increasing slabs of Rs 2.5 lakh, the rates can be 5%, 10% and so on. Therefore, someone earning Rs 12.5 lakh to Rs 15 lakh will have a tax rate of 20% for that slab. The peak rate of 30% can be charged for those earning Rs 17.5 lakh or more. A more liberal policy would be to have 30% tax for income in excess of Rs 20 lakh.

The second change could possibly be giving select deduction for the concessional regime as well. In the regular tax regime, one can reduce taxable income even by Rs 5 lakh.

Perhaps, half that value or Rs 2.5 lakh could be offered as deduction for specific avenues – employees’ provident fund (EPF), national pension system (NPS), health insurance and term insurance premiums, and perhaps housing loan principal/interest. Or, a liberal and higher standard deduction may be offered to those opting to take the new tax regime over the old one.

Probability: Since multiple reports have surfaced on incentivising the new tax regime, there is a good chance of a few tweaks being made in that direction.

Current status: The last time a major move was made dates back to 2014, when the section 80C deduction was increased from Rs 1 lakh to Rs 1.5 lakh. Also, the minimum threshold for taxability was increased to Rs 2.5 lakh and tax up to Rs 5 lakh reduced to 5%. But since then, there have been no increases in any of the deductions or exemptions. Nor has there been any serious revision in tax slabs.

Expectations: Broadly there are a few sections under which taxpayers get relief.

Section 80C: This section has a limit of Rs 1.5 lakh as the deduction limit. But it is crowded with too many investment options. These include EPF, PPF, ELSS (equity linked savings schemes of mutual funds), principal of home loan, 5-year bank fixed deposit, National Savings Certificate (NSC), SCSS (Senior Citizens’ Savings Scheme), life insurance premium and so on.

Since the last revision in the section was done 9 years ago, the expectations are that the deduction limit under this section be increased to Rs 2.5 lakh at least in light of the prevailing inflation rate.

Section 80D: This section covers health insurance premiums. For covering self and family, you get Rs 25,000 deduction from the taxable income. If you add senior citizen parents and pay premiums for them, an additional Rs 50,000 is made available.

In the aftermath of the pandemic, hospitalization claims have increased and so insurance companies have hiked health insurance premiums across the board in the last couple of years.

There is expectation that the limit on the health insurance premium of self and family would be increased to Rs 50,000.

Section 80CCD: This covers the national pension system (NPS) and allows Rs 50,000 as deduction for contributions made. Given the limited social security available and pension income would be critical for those retiring from the private sector. The government is expected to increase the limit under this section to Rs 1 lakh.

Section 24B: This part gives deduction on interest paid on home loans. The limit to interest is set at Rs 2 lakh per person for a self-occupied property. In light of the increase in interest rates on home loans to the tune of 200-250 basis points, there is expectation that this limit be increased to Rs 2.5 lakh at least to help homebuyers reduce their tax burden.

Separately, there is demand for increase in standard deduction from Rs 50,000 to Rs 1 lakh.

Probability: Going by past record, there is limited chance of most of these proposals going through. But you may never know in an election year budget, as the government may give a few concessions. However, if the primary objective is to incentivise the new tax regime, these proposals on the old rates may not go through.

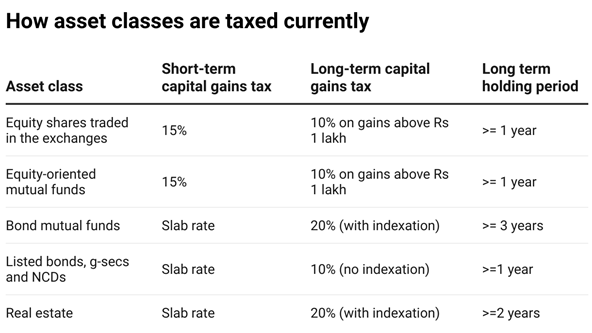

Current status: This part is perhaps the most complicated and anxiously awaited one for taxpayers, investors and various market stakeholders. Starting from the finance secretary to economists and tax experts of all hues, most have called for rationalising of capital gains taxes, holding periods and simplifying it to one structure.

Equity, debt funds, non-convertible debentures (NCDs), real estate and gold have different definitions for what constitutes long term while calculating capital gains – 1-3 years. The tax rates on capital gains are also different – 10% for equity, 20% for bonds with indexation and so on.

Expectations: There is expectation that all assets will have same holding periods to qualify as long term. Many expect it to be 3 years across asset classes. Also, indexation benefit may be offered to all asset classes than to select ones. But given that all asset classes follow different cycles and their dynamics differ vastly, there has to be considerable thought going into equalising holding periods. Even within an asset class such as debt, there are market-linked and non-linked products. Given the inherent complexities across investment avenues, a simple structure would help. However, such a structure should not ignore underlying differences.

Probability: In some form or the other, proposals on rationalising and simplifying capital gains taxation is almost certain to make it to the Budget document. Going by recent media reports, most experts are vouching for it. If there aren’t any concrete measures, there are at least likely to be hints on the directional change in the near future.

Except for watching with bated breath, there is little that an average taxpayer can do. Once you get a grip on which set of proposals go through, you can then plan your finances suitably next financial year. As with all things in life, limiting your expectations can save you from major disappointments.

Gold can react to inflation data, while crude oil may jump after an inventory report or geopolitical disruption.

Understand how crude oil trading works on MCX and also learn about contract sizes, expiry, trading hours, global benchmarks, price drivers and risks before you trade.

Learn how to calculate the break-even point in commodity trading by factoring in brokerage, taxes, and other charges

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App