Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Managing taxes is an essential skill that you should master. And once you master it, you can plan your finances more effectively. While tax savings can be realized under many sections of the Income Tax Act, this article will focus on two popular ones - the National Pension Scheme (NPS) and Equity Linked Savings Scheme (ELSS).

Additional read: Tax Saving options beyond Section 80C

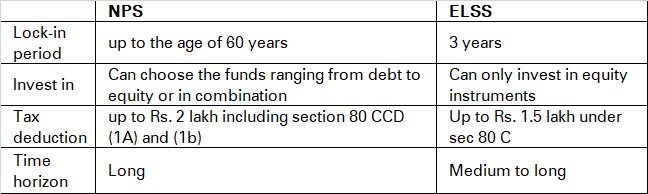

National Pension Scheme or NPS is a pension scheme that the government sponsors. It encourages individuals to save towards a retirement goal. Employees in public, private and unorganized sectors can invest in this scheme. However, it is not available for people in the armed forces.

There are two types of accounts offered under NPS – Tier I accounts and Tier-II accounts.

Tier I accounts are a primary type of NPS account and are mandatory to invest in. You can choose the different types of funds based on asset allocation as per your investment objective and risk appetite. They have a lock-in period until the age of retirement. Withdrawals are permitted only after a certain period and are subject to limitations. Tier-II accounts are voluntary accounts. However, you need to invest in a Tier I account to open a Tier II account. In addition, Tier II accounts do not have lock-in periods or withdrawal restrictions.

Investments in NPS are eligible for tax deduction under Section 80CCD (1) and 80 CCD (1B) of the Income Tax Act.

If you are currently a working professional, you likely manage your expense with your monthly salary. However, once you retire you will not receive a monthly paycheck to meet your expenses. To ensure that you are able to keep up a decent lifestyle and live your retirement days worry-free, NPS helps in building the necessary retirement corpus. The corpus serves as a source of earnings for your post-retirement life.

You do not need a lump sum amount to build your corpus. You can start investing with the funds you have in hand. You make periodic contributions as per your affordability and build your corpus systematically, without feeling burdened.

By investing in NPS you can earn incredible inflation-beating returns while at the same time managing your risk appetite. Typically, your NPS portfolio will have 75% of equity exposure. You can always adjust the equity exposure according to your risk appetite. Furthermore, your equity exposure is reduced by 2.5% every year as you near your retirement age. You earn good returns through your investment tenure.

NPS investments are classified under Section 80C of the Income Tax act. As per Section 80C, you can claim a tax benefit of Rs 1.5 lakh on your investment. Additionally, under Section 80 CCD (1B) you can claim an additional tax deduction of Rs 50,000 on your Tier 1 Account.

The Equity Linked Savings Scheme or ELSS is a tax-saving mutual fund that invests most of its funds in equity and equity-related investments. They have a lock-in period of three years which is the lowest among all other tax saving instruments. While they can be withdrawn after three years, they are better suited as long-term investments. Investment in ELSS are eligible for tax deduction under Section 80C of the Income Tax Act.

ELSS Funds are one of the finest means of wealth creation. The fund predominantly invests in various Equities and Equity linked financial instruments. This gives you a chance to earn attractive inflation beating returns.

With ELSS you have two investment options – dividend and growth option. Under the dividend option, you receive your dividends periodically. Under the growth option, you do not receive your dividends periodically but rather get reinvested. By investing in the growth option, you get to benefit from its compounding effect and maximise your returns.

Investing in ELSS is also tax-deductible. ELSS Funds are classified under Section 80C of the Income Tax Act. You can claim a tax deduction of Rs 1.5 lakh on your investment returns under this section. This ensures that you are able to enjoy your returns to the fullest, without taxation eating into them.

ELSS funds have the shortest lock-in period of all investment schemes. ELSS funds’ lock-in period is three years. This ensures your investment sum is not locked in for a long period.

|

Point of difference |

NPS |

ELSS |

|

Investment suitability |

If your goal is to create a retirement corpus, NPS is the perfect investment choice. You can build your corpus over time by making periodic contributions. |

If your goal is to earn market-adjusted returns and save on taxes, investing in ELSS is an apt choice. |

|

Tenure |

Typically, NPS investments continue until you retire or the age of 60 years, whichever comes first. |

There is no fixed tenure for ELSS funds. You can invest in the fund for any tenure. However, you are required to stay invested for the mandatory lock-in period without fail. |

|

Minimum yearly investment requirement |

The minimum yearly investment requirement for NPS varies with the type of account you hold. Generally, the minimum requirement for a Tier 1 Account is Rs 1,000, while for a Tier 2 Account is Rs 250 for a financial year. |

There are two ways to invest in ELSS Funds – lumpsum investment and via Systematic Investment Plan (SIP).

If you are investing via SIP, the minimum contribution amount differs for each fund House. Usually, the SIP minimum contribution is affordable, approximately Rs 500. |

|

Premature withdrawal facility |

You can make a premature, partial withdrawal of up to 25% from your NPS Account.

In case you wish to entirely withdraw from the investment, you can only do so after the completion of 10 years of the tenure. |

You cannot make a premature, partial withdrawal from your ELSS fund during the lock-in period.

In case you wish to make a premature withdrawal, you need to exit the investment altogether. |

|

Associated risk |

NPS is considered a lower-risk investment option in comparison to ELSS Funds. However, you must continue to be cautious of the associated risk. |

Since ELSS Funds have a high equity exposure, it is a risky investment option. |

Additional Read: What are tax saving mutual funds and how do they work?

Contributions to the NPS account are eligible for tax deductions of up to Rs. 2,00,000 – under Section 80CCD (1), they are eligible for deductions up to Rs. 1,50,000 while Section 80CCD (1B) allows an additional deduction of up to Rs. 50,000.

Moreover, upon retirement, you can withdraw up to 60% of the corpus as a lump sum tax free and the remaining 40% can be used to purchase the annuities. An annuity is a product that will provide you with a pension at a fixed rate. You can purchase the annuity by paying a lump sum amount. However, the income from annuities are taxable. With ELSS investments, if you opt for the old tax regime, you are eligible for tax deductions up to Rs. 1,50,000 per annum under section 80C of the Income Tax Act, 1961. It means you can save up to Rs. 46,800/- if you fall under the highest tax bracket of 30%. Any gains earned on ELSS investments are subject to capital gains tax.

When looking at it from a pure tax savings point of view, NPS seems like a better investment avenue given that you can claim deductions of up to Rs. 2,00,000. In comparison, ELSS allows for deductions of only up to Rs. 1,50,000. However, when choosing between the two investments, you may want to consider the other aspects.

For instance, NPS is suited to long-term investment objectives since it has a more extended lock-in period, and withdrawals are also limited whereas ELSS has a shorter lock-in period of just three years. With NPS you can choose to allocate your assets in various funds, i.e., a combination of equity and debt in your portfolio, while ELSS invests only in equity instruments.

Both NPS and ELSS are good options when it comes to tax savings. While NPS provides a higher tax deduction benefit than ELSS, the investment objectives for both vary. You need to consider your investment horizon, investment objective and risk profile when making an investment decision in either of these instruments.

Disclaimer – ICICI Securities Ltd. ( I-Sec). Registered office of I-Sec is at ICICI Securities Ltd. - ICICI Venture House, Appasaheb Marathe Marg, Prabhadevi, Mumbai - 400 025, India, Tel No : 022 - 6807 7100. AMFI Regn. No.: ARN-0845. PFRDA registration numbers: POP no -05092018. We are distributors for Mutual funds and National Pension Scheme (NPS). Mutual Fund Investments are subject to market risks, read all scheme related documents carefully. Please note, Mutual Fund and NPS related services are not Exchange traded products and I-Sec is just acting as distributor to solicit these products. All disputes with respect to the distribution activity, would not have access to Exchange investor redressal forum or Arbitration mechanism. The contents herein above shall not be considered as an invitation or persuasion to trade or invest. I-Sec and affiliates accept no liabilities for any loss or damage of any kind arising out of any actions taken in reliance thereon. Investments in securities market are subject to market risks, read all the related documents carefully before investing. The contents herein mentioned are solely for informational and educational purpose.

From supply disruptions and weather events to geopolitical developments, commodity prices move on a wide range of forces.

Understand silver trading, contract types, pricing factors, risks and expiry rules.

Additional Exposure Margin increases capital requirements for concentrated F&O securities.

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App