Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Exit load in mutual funds can be defined as the amount fund house charges an investor for redeeming or selling units of mutual funds before the stipulated period. Most of the time, this is a percentage of the investment amount and has a dual role: it discourages short-term trading but, at the same time, compensates the fund for early withdrawal of funds. The period of the exit load and percentage vary with the different schemes of mutual funds. They are very clearly defined in the offer document of the fund. Among all the conditions, it is most critical to understand the exit load charged by a mutual fund if an investor desires to effectively manage investment costs and plan redemption.

Exit load, on the other hand, is a fee charged by mutual funds when an investor sells or redeems their units before a certain period of time has elapsed. You also have to pay the exit load even if you are booking a loss when selling mutual fund units. Additionally, exit load is charged even when you are switching from one fund to another or have applied for a systematic transfer plan (STP) or systematic withdrawal plan (SWP).

This fee is typically a percentage of the amount being redeemed and is meant to discourage investors from frequently buying and selling mutual fund units, which can disrupt the fund’s management and performance.

Exit load is not charged on top of the investment amount but is simply deducted from the redemption amount. Mutual fund companies and distributors will usually tell you beforehand if they charge any exit load. Nonetheless, make sure to read the fund’s prospectus carefully if they fail to tell you.

Exit loads can vary widely depending on the mutual fund, and may be higher for funds that invest in less liquid securities or have higher management fees. It is important for investors to be aware of any exit loads associated with a mutual fund before investing and to factor this cost into their decision-making process.

Mutual fund companies, if they are charging, usually charge higher exit loads in equity funds than in debt funds because equity funds are meant for long-term investment tenures.

To calculate exit load in mutual fund you need to be aware of two things – the fees charged by mutual funds as a percentage of the redemption amount and the exit load period. You also need to be aware of the net asset value (NAV) of the fund.

Let us assume there is an equity fund that charges 1% of the redemption amount as the exit load in case you redeem your investment within one year of investing. There are two scenarios here: lump sum investment and SIP investment.

In the case of lump sum investment, the calculation is fairly simple. Let us assume that you bought 1,000 units of the aforementioned mutual fund at a net asset value (NAV) of Rs 50. In five months or 150 days, you sold your entire investment at a NAV of Rs 55.

Your initial investment amount was Rs 50 x 1,000 units = Rs 50,000. In five months, the value of the fund is Rs 55 x 1,000 units = Rs 55,000. However, since you are selling the investment, and there is an applicable exit load, the redemption amount will be different:

Exit load: 1% of (Rs 55 x 1,000) = Rs 550. This amount will be deducted from the value of the investment at the time of redemption.

The eventual redemption amount will be Rs 55,000 – Rs 550 = Rs 54,450.

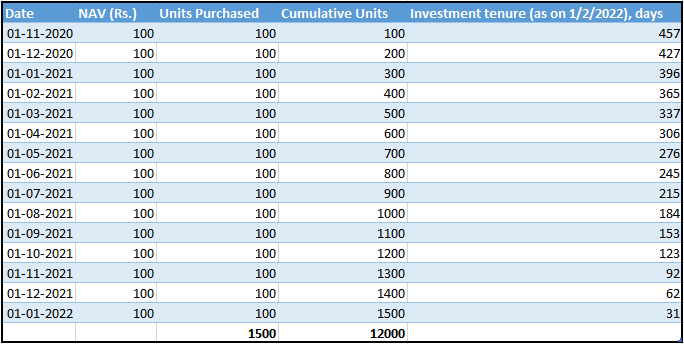

In the case of investment via systematic investment plan (SIP), the calculation is a little trickier given the NAV and period of investment vary for each instalment. For the sake of calculation, let us assume, you keep buying 100 units of the aforementioned fund at an average NAV of Rs 100 per unit. You start your SIP in November 2020 and continue it until January 2022.

Now, you need money in February and plan to sell 1,000 units from the fund on February 1, 2022. In SIP withdrawals, the oldest bought units are sold first. Thus, the exit load will not be applicable on the entire sale but only on those units that are yet to complete 365 days.

From the table above, we can see first 400 units have completed 365 days or more. Thus, there will be no exit load on this. Exit load will be applicable on the next 600 units that you have sold.

Exit load = 1% of (units x NAV)

= 1% of (600 x 100)

= Rs 600

Hence the total redemption amount will be,

= Rs (1000 x 100) – 600

= Rs 100000 – 600

= Rs 99,400

Though exit loads of mutual funds sound like a penalty, they can support long-term investing. Following are the different types of exit load available:

To avoid exit loads in mutual funds, hold your investment for the minimum lock-in period mentioned in the scheme details. Choose funds with a short lock-in period or no exit load at all if you need more flexibility.

Remember, not all funds come with exit loads. Do check with fund details before you invest in them.

Why is exit load levied on mutual funds?

Mutual funds charge an exit load to prevent short-term trading. If not checked, such early redemption is prone to disrupt the strategy of a fund and impact long-term investors. The fee encourages you to stick for the long haul, which aligns with mutual funds' goals.

When is exit load applicable?

Exit load applies when you redeem your mutual fund units before a specific period, typically 1-2 years. It's like a fee for early withdrawal. Check your fund's details to see the exact exit load window.

What is entry load and exit load in mutual funds?

Entry and exit loads are fees in mutual funds. Entry load is a charge you pay to buy units (rare these days). Exit load is a fee for selling units before a certain time (like an early withdrawal penalty). Both aim to encourage long-term investing.

Will I would be required to pay exit load if I choose the SWP option?

No, typically exit loads don't apply to SWP (Systematic Withdrawal Plan). SWP lets you withdraw invested amount regularly, and it's treated as selling your units gradually. So, you benefit from long-term investment without the exit load penalty.

What is a good exit load for mutual funds?

The best exit load for a mutual fund is actually zero! It reduces your returns. However, some funds have them. Look for funds with low or no exit loads, especially if you might need to access your money sooner.

What is the exit load if I switch from one mutual fund scheme to another in the same Asset Management Company?

Switching funds within the same AMC might still trigger an exit load. It's seen as a redemption (selling) of the old fund. Check the exit load period of the original fund to see if you'll be charged.

Learn how to calculate the break-even point in commodity trading by factoring in brokerage, taxes, and other charges

Learn how ICICI Direct's Auto Order Slicing automatically splits large commodity orders for faster, seamless execution while complying with exchange limits.

Learn about a BSDA account, its eligibility criteria, annual maintenance charges, and the latest SEBI rules for Basic Services Demat Accounts.

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App