Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Every year, with the introduction of the union budget comes the question - What are my stocks going to be taxed at? The answer this year is that there is no change in capital gains tax for financial assets such as Stocks, Mutual Funds etc. in Budget 2023.

With no changes in the capital gains in budget presented by Finance Minister Nirmala Sitharaman, let’s have a look at the history of capital gains taxation in India.

History of Capital Gains taxation in India

Capital gains are profits earned by an investor on selling of assets in the capital markets. Any stock held for more than one year is considered under Long Term Capital Gains(LTCG) tax. For stocks held under one year is considered under Short Term Capital Gains(STCG) tax.

Currently, capital gains are taxed at 10% for Long Term Capital Gains (exempt up to ₹1lakhs), and 15% for Short Term Capital Gains.

Now let’s understand the current tax regime with an example:

Short term capital gain tax

Mr A bought 100 shares of Larsen & Toubro ltd at Rs 950 per share on 8th June2020 and sold the same 100 shares of Larsen & Toubro at Rs 1500 per share on 15th February 2021 within 1year (less than 12 months).

LARSEN AND TUBRO (INE018A01030), HOLDING PERIOD = 8 MONTHS 6 DAYS

|

Stock Name |

BUY VALUE |

SALE VALUE |

GAIN (SALE-BUY) VALUE |

|

LARSEN & TOUBRO |

95,000 |

1,50,000 |

55,000 |

Gain on Larsen & Toubro is Rs. 55,000/-.

Short term capital gain tax = 55000 X15% = 8250.

Long term capital gain tax

Mr P bought 200 shares of Titan Ltd. At Rs 820 per share on 27th November 2017 and sold the same 200 shares of Titan at Rs 1700 per share on 1st July 2021

TITAN (INE280A01028), HOLDING PERIOD= 3 YEARS 8 MONTHS

|

Stock Name |

BUY VALUE |

SALEVALUE |

GAIN (SALE- BUY) VALUE |

|

TITAN |

164000 |

340000 |

176000 |

Long Term Capital Gain = 176000 (Up to Rs 100000 is not taxed as per the provision)

Long term capital Gain Tax= (176000-100000) = 76000 X 10% = 7600

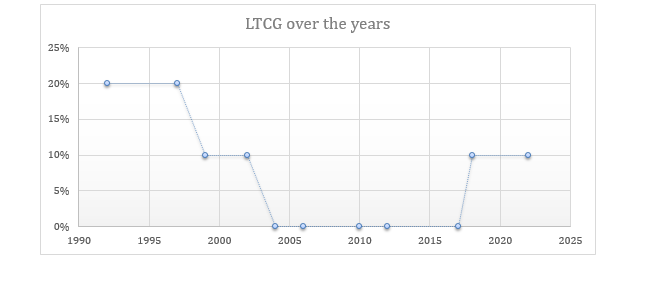

Dividend Tax History:

|

1992 |

Taxed in the hand of the shareholder |

|

1997 |

Exempt |

|

1999 |

Exempt |

|

2002 |

Taxed in the hand of the shareholder |

|

2003 |

Exempt |

|

2016 |

10% for dividends more than ₹10 lakhs |

|

2020 onwards |

Taxed in the hand of the shareholder |

How are losses treated & can it set off against future profit?

Any Unadjusted losses can be carried forward up to 8 years. However, if there is any capital loss, then file it before due date to carry forward the loss and then set off from the capital gains arising in future. Short term capital loss can be carried forward up to 8 years and can be set off against short term capital gain and long-term capital gain before taxation. Long term capital loss can be carried forward for up to 8 years and can be set off against long term capital gains only before taxation.

What are taxation on equity intraday transactions?

Intraday-day trading (speculative business income)- If the shares are bought and sold regularly in a short duration then this is not considered to be under capital gains but under speculative business income as per income tax section 43(5). The gain from this type of income is taxed under business income and is taxed as per the assesses tax slab rate.

Long term Capital Gain= Sale value - Cost of acquisition

What is concept of Grandfathering? Can you explain with an example that how long term capital gains will be calculated on sale of shares? What will be the cost of acquisition?

Sale value means the consideration received on the sale of equity share. The concept of Grandfathering means that any gain calculated upto 31st Jan 2018 i.e. taking the highest price of the stock as on Jan 31, 2018, will not be chargeable to tax. This price as on Jan 31, 2018 is the fair market value as on Jan 31, 2018.

Gains on stock after Jan 31, 2018, will be chargeable to tax of 10% provided the shares are sold on or after April 1, 2018. Please note, If the shares are sold on or upto March 31, 2018, any long term capital gain will be exempt from tax.

What is Tax Loss Harvesting-?

Tax-loss harvesting is the practice of selling a share that is incurring a loss, so that by realizing the loss, you can offset the same against realized gain for the same year and save on taxes. The security has to move out of the demat account by delivery sell transaction and the sold security is replaced by the same or a similar security.

Gains from F&O are not considered capital gains but business income. As these are considered non-speculative business gains, income tax is levied according to the applicable tax slab rates.

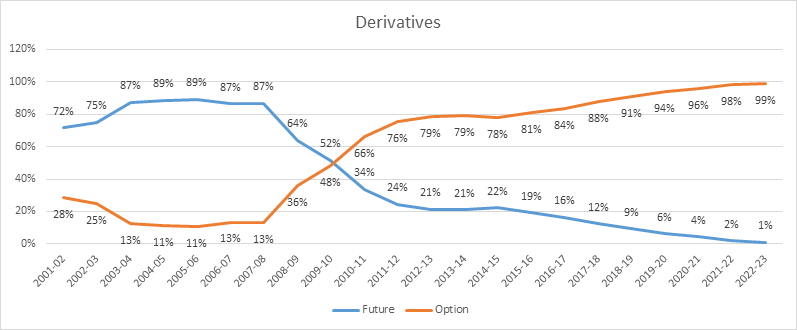

History of STT on Derivatives:

Equity and derivatives transactions in the stock exchange have been attracting securities transaction tax (STT) since 2004. There have been substantial changes in STT rates after that - For example, the rates of STT on equity and on F&O have been substantially brought down compared to what they were in 2004. Secondly, there has been a fine tuning of the definition of volumes in case of derivatives.

So, while the STT on futures transactions is still imposed on the notional value of the transaction, the STT on options transactions is imposed on the premium value of the transaction. With effect from September 1, 2019 where options are exercised, STT at the prescribed rate are levied on the intrinsic value instead of the settlement price as that was before. Further with regards to intrinsic value has been defined as the difference between the settlement price and the strike price of the options

The above Graph shows the contribution of Future and options towards equity derivatives turnover. We can see how the share of futures with a peak of 89% in 2004-05 has constantly moved down to 1% in recent times.

The STT payable on 1 lot of options is substantially lower than the STT payable on 1 lot of futures. This is despite the fact that the STT on options had been recently hiked 3-fold from 0.017% to 0.05%. The reason is that options are charged STT on their premium value while futures are charged STT on their notional value. This has been one of the key reasons for the rapid growth of option volumes in India.

For immovable property, LTCG is considered for assets held for more than 24 months. For Gold, it is considered for gold held over 36 months. Tax rate being 20% for both.

Mutual funds are taxed as per the category they fall in. Different type of mutual funds and their applicable tax rates are mentioned below.

|

Fund Type |

Short-term capital gains |

Long-term capital gains |

Tax Rate |

|

Equity funds |

Shorter than 12 months |

12 months and longer |

STCG: 15% LTCG: 10% (exempt up to 1 lakh) |

|

Debt funds |

Shorter than 36 months |

36 months and longer |

STCG: Tax Slab Rate LTCG: 20% |

|

Hybrid equity-oriented funds |

Shorter than 12 months |

12 months and longer |

STCG: 15% LTCG: 10% (exempt up to 1 lakh) |

|

Hybrid debt-oriented funds |

Shorter than 36 months |

36 months and longer |

STCG: Tax Slab Rate LTCG: 20% |

(Source: Cleartax)

What are Securities Transaction Tax (STT)?

STT is a kind of financial transaction tax which is similar to tax collected at source (TCS). STT is a direct tax levied on every purchase and sale of securities that are listed on the recognized stock exchanges in India.

|

Taxable securities transaction |

Rate of STT |

Person responsible to pay STT |

Value on which STT is required to be paid |

|

Delivery based purchase of equity share |

0.10% |

Purchaser |

Price at which equity share is purchased* |

|

Delivery based sale of an equity share |

0.10% |

Seller |

Price at which equity share is sold* |

|

Delivery based sale of a unit of oriented mutual fund |

0.00% |

Seller |

Price at which unit is sold* |

|

Sale of equity share or unit of equity oriented mutual fund in recognised stock exchange otherwise than by actual delivery or transfer and intra day traded shares |

0.03% |

Seller |

Price at which equity share or unit is sold* |

|

Derivative – Sale of an option in securities |

0.02% |

Seller |

Option premium |

|

Derivative – Sale of an option in securities where option is exercised |

0.13% |

Purchaser |

Settlement price |

|

Derivative – Sale of futures in securities |

0.01% |

Seller |

Price at which such futures is traded |

|

Sale of unit of an equity oriented fund to the Mutual Fund – Exchange traded funds (ETFs) |

0.00% |

Seller |

Price at which unit is sold* |

|

Sale of unlisted shares under an offer for sale to public included in IPO and where such shares are subsequently listed in stock exchanges |

0.20% |

Seller |

Price at which such shares are sold* |

|

PURCHASE OF UNITS OF EQUITY ORIENTED MUTUAL FUNDS |

NIL |

PURCHASER |

NA |

(Source: Cleartax)

Gold can react to inflation data, while crude oil may jump after an inventory report or geopolitical disruption.

Understand how crude oil trading works on MCX and also learn about contract sizes, expiry, trading hours, global benchmarks, price drivers and risks before you trade.

Learn how to calculate the break-even point in commodity trading by factoring in brokerage, taxes, and other charges

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App