Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Not all demat accounts are the same. Here we not only look at the demat account types but also the basis of classification. The types of demat accounts can be based on cost, repatriation and linkages. Today, investors have access to different types of demat account online and they can choose the one best suited to them. Here is a quick look at the different types of demat account available in India, the features and their classification rationale.

As Shakespeare would have said, “A rose is a rose is a rose”. After all, whatever you type of demat account you have, it would still holds shares and other securities. It is not as simple as that. In India, different types of demat accounts can be classified based on residency, the level of service, on repatriation status and backward and forward linkages. Let us take a look at the different types of demat account:

The name itself is suggestive in this case. The Resident demat account is held by Resident Indians as defined in the Income Tax Act based on the number of days of residency. People who do not satisfy these criteria would either be Resident but not Ordinarily Residents or Non-Residents (NRIs). The NRI demat account is distinct from a resident account in the sense that the KYC of the NRI demat account must include India related documents and also documents to establish residency in the country of domicile abroad.

Also, non-resident demat accounts can be either repatriable or non-repatriable demat accounts and we shall look at this point in much greater detail later. If you have opened a resident demat account and become an NRI subsequently, then the resident demat account has to be converted into an NRO demat account, so as to reflect the status of the individual.

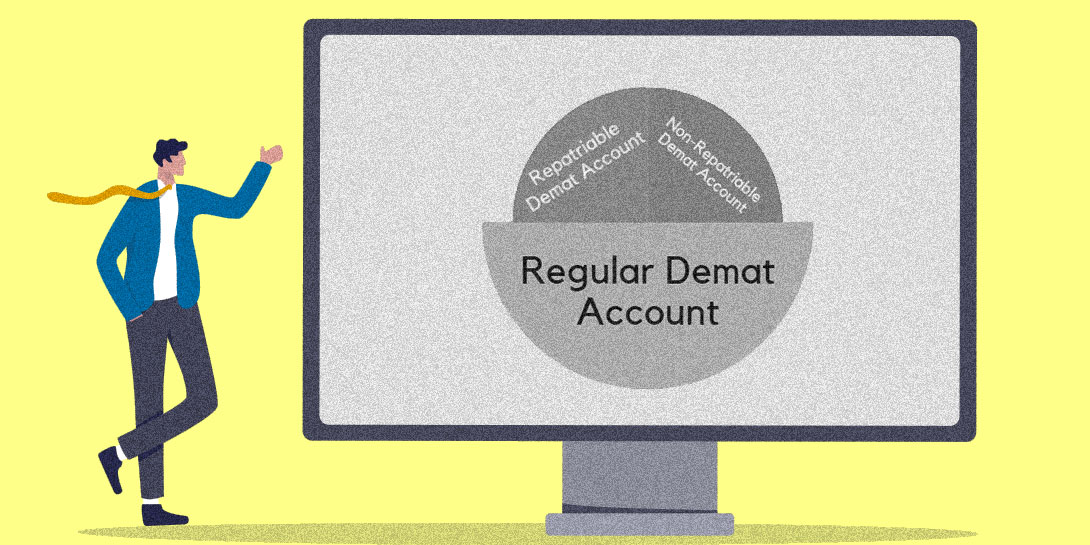

Regular demat account is one of the default demat account types for resident Indians. It is the most common form of demat account and is used by people residing in India and holding Indian citizenship. Regular demat account will necessarily charge annual maintenance charges (AMC), although account opening charges are waived off. The fees charged for a regular type of demat account depends on the value of securities held in the account. A regular demat account can be with NSDL or with CDSL. There is no upper limit to the value of the holdings in your regular demat account.

Let us now turn to the BSDA demat account. The Basic Services Demat Account (BSDA) is a low cost demat account targeted at small investors with a small portfolio of under Rs 10 lakhs. SEBI had introduced BSDA to offer customers an alternative to high demat costs. In most ways, the regular demat account and BSDA are almost similar except that BSDA does not impose any annual maintenance charges (AMC). In BSDA, you pay zero AMC if the value of holdings is up to Rs 4,00,000. A nominal fee of Rs100 is charged for BDSA with value of between Rs 4 lakhs and Rs 10 lakhs. Beyond Rs 10 lakh value, BSDA automatically gets shifted to a regular demat account.

Repatriable demat account and non-repatriable demat account is applicable to NRI demat accounts. Repatriation is the ability to freely remit money abroad. To open a repatriable demat account, the NRI must have an NRE bank account linked to demat account. Investors residing outside India can transfer funds abroad with a repatriable demat account. To open Repatriable Demat Account, NRI must provide documents like copy of passport, PAN card, copy of Visa, overseas address proof, passport size photograph and FEMA declaration; apart from a cancelled cheque leaf of NRE account.

NRIs with non-repatriable demat accounts cannot transfer shares abroad freely. Non-repatriable demat account are linked to an NRO (non-resident ordinary) bank account. NRIs are permitted to hold up to 5% of paid-up capital in an Indian company. In an NRO linked non-repatriable demat account, there are restrictions on repatriation of funds. While NRE accounts are for funds earned abroad, NRO account are for funds earned within India.

This is not exactly a category of demat account, but more a comparison of linkages between trading account, demat account and bank accounts. Two-in-one demat accounts are very popular and are offered by brokers who also double up as DPs. The Three-in-One account is offered by bank-affiliated brokers ICICI Direct and HDFC Securities; wherein the bank account, trading account and demat account are a seamless chain.

Gold can react to inflation data, while crude oil may jump after an inventory report or geopolitical disruption.

Understand how crude oil trading works on MCX and also learn about contract sizes, expiry, trading hours, global benchmarks, price drivers and risks before you trade.

Learn how to calculate the break-even point in commodity trading by factoring in brokerage, taxes, and other charges

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App