Download

iLearn application

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

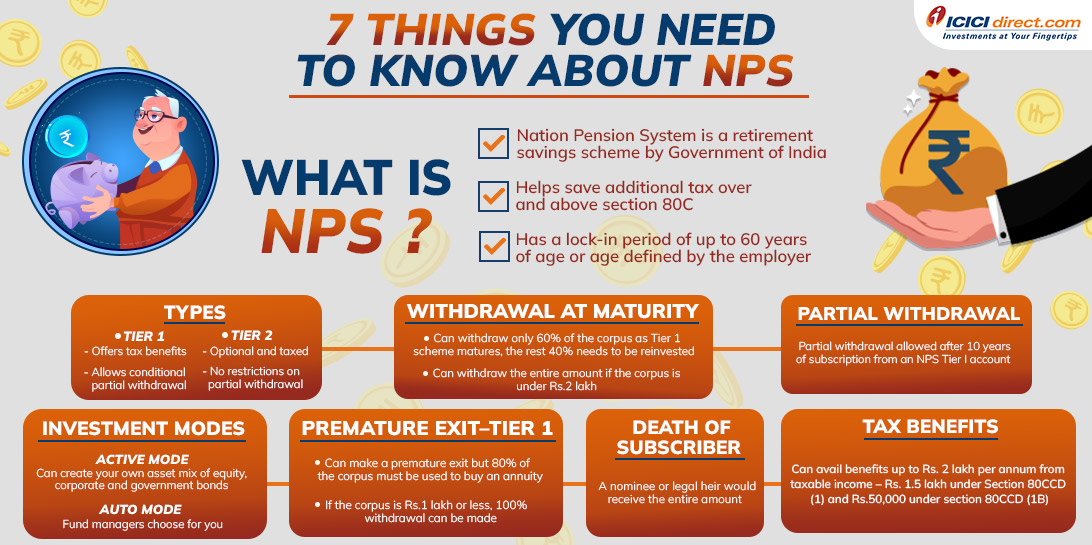

Most of us worry about retirement and having enough income in our old age. While some people save and invest enough, there are many who find it difficult to manage finances to ensure enough money post-retirement. The National Pension System (NPS) is a good option for those who want income after their working years are over.

NPS is a contribution-based pension scheme aimed at providing a regular income after retirement. It was launched for government employees in 2004 and later opened to everyone in 2009 through a few select banks, including ICICI Bank.

Contributions to NPS are handled by fund managers who follow guidelines set by the Pension Fund Regulatory and Development Authority (PFRDA) to invest in a diversified set of instruments comprising government bonds, T- bills, corporate debentures and shares.

The amount invested in NPS has a lock in period till the subscriber turns 60 or age defined by the employer. Some people find the long lock-in and compulsory annuity undesirable, but many point out that it is fundamentally a pension scheme, and hence withdrawal must be discouraged.

Click here to invest in NPS through ICICIdirect.

Learn how to calculate the break-even point in commodity trading by factoring in brokerage, taxes, and other charges

Learn how ICICI Direct's Auto Order Slicing automatically splits large commodity orders for faster, seamless execution while complying with exchange limits.

Learn about a BSDA account, its eligibility criteria, annual maintenance charges, and the latest SEBI rules for Basic Services Demat Accounts.

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App

Elevate Your Financial Knowledge with the

ICICI Direct iLearn App