Invest

Invest

Learning Modules Hide

Hide

Chapter 8: Advanced Concepts in Futures

Aisha is a stock market trader who is exploring the world of Futures for the first time. She enters into a contract to sell a lot of Nifty Futures contracts. The price is slightly higher for the near month contracts than the underlying index and even higher for subsequent two months. She hears that the Open Interest is higher for the near-month contract and lower for farther months. She also comes across terms like Rollover and Spread.

Since Aisha is new to these terms, she wants to understand what they mean. Let’s break these down for her, shall we?

Open Interest in Futures contracts

Open Interest is a term that is often used in the world of derivatives. It indicates the number of contracts that are due or active in the market and are yet to be settled.

Note: A single contract accounts for both parties, a buyer and a seller, involved in the transaction. The number of Open Interest, therefore, refer to the number of active contracts rather than the number of active parties in the market.

The higher number of open positions of a particular Futures contract denotes that the contract is highly active and has even higher participation.

Now, you might be wondering how Open Interest rises and falls. Aisha has this doubt too. Let’s understand this with an example:

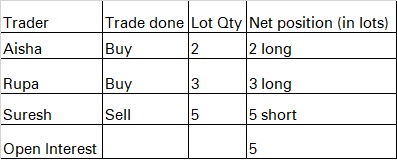

Let’s suppose the following transactions happen on day 1:

- Aisha buys 2 lots of Nifty Futures contracts and his net outstanding position is 2 lots long.

- Rupa buys 3 lots of Nifty Futures contracts and his net outstanding position is 3 lots long.

- Suresh has sold 5 lots of Nifty and his net outstanding position is 5 lots short

- So the total no. of outstanding contracts is 5, so Open Interest is 5.

Let’s suppose the following transactions happen on day 2:

- Aisha sold her 1 lot of Nifty and his net outstanding position is 1 lot long.

- Rupa sold her 3 lots of Nifty Futures contract and his net outstanding position is zero.

- Suresh has bought 2 lots of Nifty and his net outstanding position is 3 lots short.

- Charles has purchased 2 lots of Nifty and his net outstanding position is 2 lots long.

- So the total no. of outstanding contracts is 3 and so Open Interest is 3.

Question: Which parties remain in the Open Interest Futures contract now in the example above? Aisha, Suresh and Charles remain in the Open Interest on day 2.

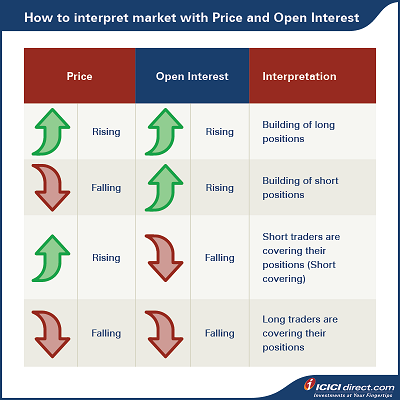

- Open Interest can also be used to understand market movement but not give any sense of whether the market will move up or down.

- Rising Open Interest supported by rising prices is an indication of a building of long positions. Conversely, increasing Open Interest and falling prices are a sign of a building short positions.

- Falling Open Interest along with rising or falling stocks is a sign of position covering. Rising prices with falling Open Interest signify that short traders are covering their positions, also known as short covering. Falling prices with falling Open Interest is a sign that long traders are covering their position.

Rollover and Rollover percentage

Now, on the day of derivatives expiry on the last Thursday of a month, Aisha chooses to Rollover or carry forward her position.

At the expiry of one Futures position, the participants may square off their current contract position and shift onto the next series with the same original position. When you Rollover a Futures contract, the price difference between both the series at the time of Rollover must be settled.

E.g., Rupa has a long position in one lot (75 Qty) of Futures of Nifty for the current month. She sees some more upside left in the near Future. She decides to Rollover the position to the next month and pays the difference in the prices of both contracts. If a current month's nifty contract price is Rs. 14110 and next month's price is Rs. 14,150. She needs to pay the difference in the price, i.e. (14150-14110) *75 = Rs. 3,000

Rollover percentage, on the other hand, is calculated by dividing the next month and the far month contracts from the total Futures contracts available in the underlying asset and then multiplied by 100. High Rollover percentage indicates that current momentum will continue.

Rollover percentage = {(Next month Open Interest + Far month Open Interest) / (Near month Open Interest + Next month Open Interest + Far month Open Interest)} *100

Spread position

A Spread position in a Futures contract involves taking simultaneous opposite positions in two contracts to benefit from the price discrepancy of the two. The underlying asset in the two contracts is the same.

For example, let’s take Aisha’s contract. The current price of Nifty Futures for July 2021 expiry Rs 15670 per unit. Rupa believes the price might increase to 15800 but not beyond 15900. Rupa takes a long position in the 1-month Futures contract and a short position in the 3-month Futures contract. This strategy is called Calendar Spread.

- There may be a large difference in the Futures prices in two consecutive months. When that deviation in Future prices happens from the fair value is large, a Spread position can be taken. The contract which is overvalued must be sold and simultaneously the contract of the adjacent month should be bought.

- In a Spread position, both the positions need to be closed simultaneously, otherwise the single position will be considered a naked position and require a higher margin in comparison to the Spread position.

Margin and risk involved in a Spread position in Futures contract

The Spread position value is calculated by multiplying the weighted average price of the position in a far month contract and Spread position quantity.

Spread margin percentage is then applied to the Spread position value to arrive at the Spread margin. The only risk the trader is exposed to is basis risk. In simple terms, the basis is the difference between the prices of two positions. In the Calendar Spread example, the basis risk can be calculated as below:

Basis = Futures price of two months - Futures price of one month

The risk for the Calendar Spread is that the basis amount might not remain constant, which means that the price of two months or one month might change unexpectedly, leading to a change in the basis.

Is it better to take a Spread Futures position in comparison to a single Futures contract?

Yes, trading through Spread positions can hedge the risk when compared to taking a position in a single Futures contract. Every Spread position is a hedge position as simultaneous buying and selling is done in two different Futures contracts (of the same underlying) of two maturities. You hedge your buy position by a sell position in a subsequent month or vice versa.

Secondly, margin requirements will also reduce when a trader opts for Spread trading strategies. However, do note that as Spread positions have less risk, the probability of profit is also less.

Summary

- Open Interest is the number of contracts that are due or active in the market and are yet to be settled.

- A single contract, with a buyer and a seller, is accounted for as one Open Interest contract.

- Rising Open Interest supported by rising prices is an indication of a building of long positions. Conversely, increasing Open Interest and falling prices are a sign of a building short positions.

- The process of extending or carrying forward a Futures position to another position with a new expiry date is called Rollover.

- When you Rollover a Futures contract, the price difference between both the series at the time of Rollover has to be settled.

- Rollover percentage is calculated by dividing the next month and the far month contracts from the total Futures contracts available in the underlying asset and then multiplied by 100.

- A Spread position in a Futures contract involves taking simultaneous opposite positions in two contracts to benefit from the price discrepancy of the two. The underlying asset in the two contracts is the same.

Now you know some advanced concepts related to Futures contracts. In the next chapter, we will examine the different players in a Futures contract and their role in a contract.

Disclaimer:

ICICI Securities Ltd. ( I-Sec). Registered office of I-Sec is at ICICI Securities Ltd. ICICI Venture House, Appasaheb Marathe Marg, Prabhadevi, Mumbai - 400 025, India, Tel No : 022 - 6807 7100. I-Sec acts as a Composite Corporate agent having registration number –CA0113. PFRDA registration numbers: POP no -05092018. AMFI Regn. No.: ARN-0845. We are distributors for Mutual funds and National Pension Scheme (NPS). Mutual Fund Investments are subject to market risks, read all scheme related documents carefully. Please note, Mutual Fund and NPS related services are not Exchange traded products and I-Sec is just acting as distributor to solicit these products. Please note, Insurance related services are not Exchange traded products and I-Sec is acting as a corporate agent to solicit these products. All disputes with respect to the distribution activity, would not have access to Exchange investor redressal forum or Arbitration mechanism. The contents herein above shall not be considered as an invitation or persuasion to trade or invest. I-Sec and affiliates accept no liabilities for any loss or damage of any kind arising out of any actions taken in reliance thereon. Investments in securities market are subject to market risks, read all the related documents carefully before investing. The contents herein mentioned are solely for informational and educational purpose.

COMMENT (0)