Invest

Invest

Agrochemicals company UPL announced Q3FY24 & 9MFY24 results:

- Q3FY24:

- Revenue of Rs 9,887 crore, representing a YoY decrease of 28% from Rs 13,679 crore in Q3FY23.

- Profit for the quarter stood at Rs 2,689 crore, showing a YoY decrease of 54% from Rs 5,831 crore in the same quarter of the previous year.

- Contribution margin witnessed a decline from 42.6% in Q3FY23 to 27.2% in Q3FY24, reflecting a decrease of 1540 basis points (bps).

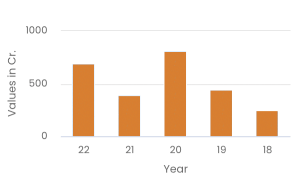

- EBITDA for Q3FY24 was Rs 416 crore, marking an 86% YoY decrease from Rs 3,035 crore in Q3FY23.

- EBITDA margin also experienced a substantial decline, dropping from 22.2% in Q3FY23 to 4.2% in Q3FY24, representing a reduction of 1800 bps.

- 9MFY24:

- Revenue was Rs 29,020 crore, showing a YoY decrease of 22% from Rs 37,007 crore in 9MFY23.

- Profit for 9MFY24 was Rs 10,847 crore, reflecting a YoY decrease of 32% from Rs 15,889 crore in 9MFY23.

- Contribution margin decreased from 42.9% in 9MFY23 to 37.4% in 9MFY24, indicating a decline of 556 bps.

- EBITDA for 9MFY24 was Rs 3,583 crore, representing a YoY decrease of 56% from Rs 8,145 crore in 9MFY23.

- EBITDA margin dropped from 22.0% in 9MFY23 to 12.3% in 9MFY24, reflecting a decrease of 966 bps.

Commenting on the Q3FY24 performance, Mike Frank, CEO – UPL Corporation, said, “Destocking continued to weigh down the global agrochemical market. Overall, prices remained stable QoQ in the crop protection business but came off significantly vis-à-vis the high base of the previous year amid intense post-patent price competition. Given this backdrop, our Q3 performance was significantly impacted by these headwinds in line with the rest of the industry, which is currently experiencing its worst downturn in decades.

However, we did see a pick-up in volumes in Latin America, and a double-digit growth in revenue in the RoW region. Our high-margin differentiated and sustainable portfolio continued to outperform as the revenue share of this portfolio increased to 37% of crop protection revenue (ex-India) vs 28% last year. Contribution margins too were down only marginally versus last year adjusted for the short-term impact of high-cost inventory liquidation and higher rebates to channel partners.

We continued to implement cost optimization initiatives to align our operations with the new reality, reducing SG&A expenses by 19% YoY in Q3. We are well on track to reduce our SG&A by $100 million in FY25 (from the base of FY23). Going forward, while we are optimistic about a progressively improved performance in Q4FY24 and Q1FY25, we expect normalized business performance from Q2FY25. Our foremost priority is reducing debt. In line with this, we have also recently announced a rights issue of up to $500 million and are exploring capital raise opportunities at platforms in addition to operational cash flows.”