Bond yield is the return an investor realizes on a bond. It is the anticipated return on an investment, expressed as an annual percentage. For example, a 8% yield means that the investment averages 8% return each year till maturity. Yield is an important concept in bond investing. It is used to measure return of one bond against another and it enables investors to make informed decision while investing in bonds.

Yield is commonly measured in two ways, current yield and yield to maturity.

A) Current yield

The current yield is the annual return on the investment value of bond, regardless of its maturity. If you buy a bond at par, the current yield equals its coupon rate. Thus, the current yield on a par-value bond paying 8% is 8%. However, if the market price of the bond is higher or lower than par, the current yield will be different. For example, if you buy a Rs. 1000 bond with a 8% stated interest rate at Rs. 1100, your current yield would be 7.27% (Rs. 1000 x 0.08/Rs.1100).

B) Yield to maturity

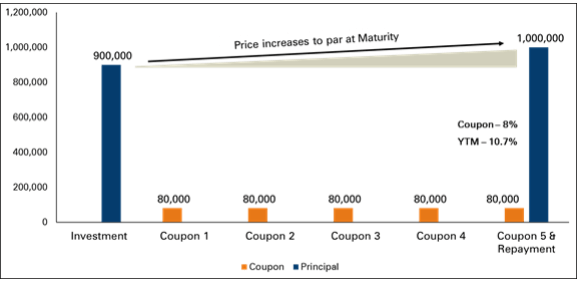

It is the total return an investor receives on a bond if held until maturity. It enables one to compare bonds with different maturities and coupon rates. Yield to maturity includes the current yield and the capital gain or loss you can expect if you hold the bond to maturity. If you pay Rs. 900 for a 5% coupon bond with a face value of Rs. 1,000 maturing five years from the date of purchase, you will earn not only Rs. 50 a year in interest but also another Rs. 100 when the bond’s issuer pays off the principal. By the same logic, if you buy that bond for Rs. 1,100, representing a Rs.100 premium, you will lose Rs. 100 at maturity.

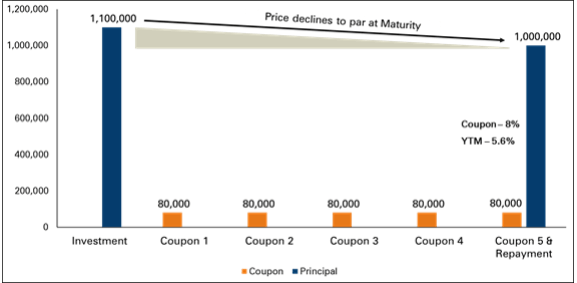

Example 1 - YTM illustration of a 5 year bond with 8% annual interest bought at Premium and held till maturity

Example 2 - YTM illustration of a 5 year bond with 8% annual interest bought at discount and held till maturity